Recently Zerodha, the leading discount broker in India has come up with a direct mutual fund platform called COIN. While we are paying a hefty commission to the mutual fund-certified agents, COIN can save us from paying all those charges. In this post, I shall discuss the Zerodha Coin review and also take you through the Zerodha Coin charges.

Before you know more about Zerodha Coin review, you must have a Zerodha trading account to proceed. You can apply for a Zerodha account by providing your name, phone number, and email id in the form below and we will assist you in account opening. The account opening process is generally instant for KYC holders, for others it can take as much as 3 days.

What is Zerodha Coin?

As we discussed ZERODHA COIN is India’s first direct mutual fund platform. People don’t know about direct mutual funds much. Every mutual fund can be bought either in the regular plan or in the direct plan. A portion of the AUM is invested in the regular plan and another portion is invested in the direct plan. COIN is the platform where you can purchase funds through the direct route.

Zerodha Coin Review

Let us now review the Zerodha Coin platform starting from how to log in, how to invest, returns prospect, etc.

Zerodha Coin Login Process:

- Visit coin.zerodha.com by clicking here.

- On the top right, there is a login link. Click it and you can log in with Zerodha Kite credentials.

- You will be redirected to the Zerodha Coin dashboard and start buying direct mutual funds.

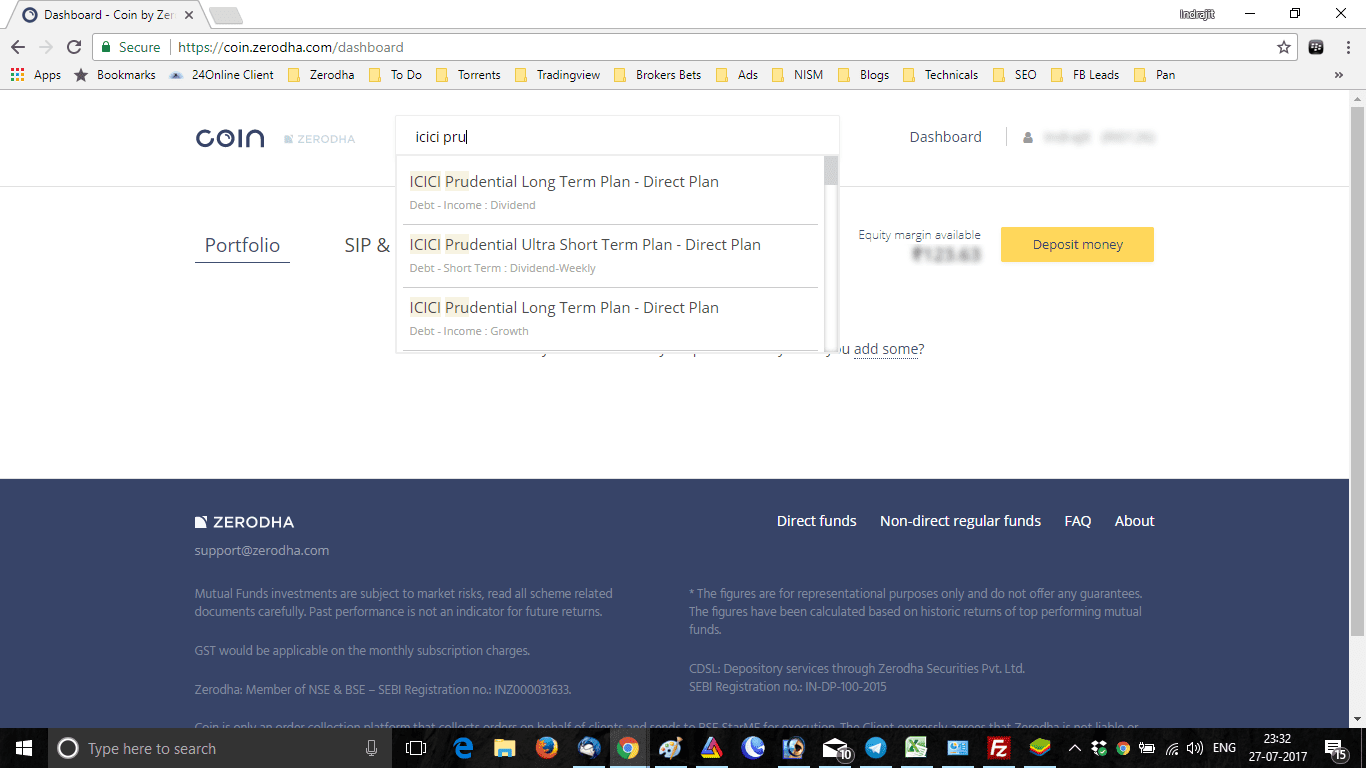

How To Invest In Mutual Funds Through Zerodha Coin?

Once you are logged into the COIN dashboard you can search for your favorite mutual fund and invest in it. Watch the image below:

Once you search for your favorite mutual fund you can check its NAV, and equity curve, find returns of the last 1 year, 3 years, and 5 years and there are two options for purchasing the best mutual funds. You can invest lump sum using the BUY button or you can also invest through a systematic investment plan.

What Are Zerodha Coin Charges?

There is a difference between charges in a regular plan and a direct plan of a Mutual Fund. For example, in a fund, the expense ratio in the regular plan is 2.36% whereas, in the same fund, the expense ratio in the direct plan is only 1.06%. Why is the difference in this expense ratio? This is because distributors sell regular plans. The agents, the banks, etc act as an intermediary in mutual funds.

So, Zerodha Coin charges or direct mutual funds charges are only different from a regular plan by 1% or so. Is it a big deal? Let’s check how this 1% can make a difference.

Example of Returns from a Direct Mutual Fund

Suppose you invest Rs. 10000 every month for 25 years, your total invested amount is Rs. 10 lacs. At the rate of return of 15% per annum, your ending capital will be Rs. 32840737 (3.3 Crores). Now if the rate of return becomes just a percent higher, i.e. 16%, your return will be Rs. 39652178 (4 Crores). So it’s a huge difference in ending capital in just a 1% increase in the rate of return. So low Zerodha Coin charges play a major role for long-term investors.

FAQs on Zerodha Coin Review

Yes, Coin by Zerodha is a very secure platform for investing in direct mutual funds. They use bank-level security measures to ensure that your transactions are safe and secure.

Yes, you can invest without paying any extra charges through Coin by Zerodha. There is absolutely no fee involved for making transactions on the platform and there are no extra taxes or any sort of hidden fees applied.

Through Coin, you get access to direct mutual fund plans which provide lower expense ratios than regular plans along with assured returns over time. You also get detailed financial insights allowing you to manage your investments better while getting help if required from their expert advisors who will guide you through each step along the way.

The Coin makes its money through the commission it takes when users sell units of mutual fund schemes on its platform, as well as interest earned in savings accounts maintained with major nationalized banks like ICICI Bank, SBI, etc., where all user holdings are held completely safe.

Conclusion

In my Zerodha Coin review, I find this platform a really new and money-saving concept for mutual fund investors. You can ask more queries on COIN in this post at the Trading QNA site, where the Zerodha guys try to answer your queries fast.