Overview

Straddle and Strangle in options are strategies of the two most common options strategies for traders. Straddle and strangle in options are standard strategies for traders in the event of impending big moves in stocks or indices. Though it seems amusing, these two common English words originate from the wrestlers’ arena!

Options are financial derivatives of the underlying. The value of options largely depends upon the value of the underlying stocks, their price fluctuations, and other factors like days to expiry and volatility. Options traders buy Calls and Puts or write them to take advantage of price fluctuations. Options traders use options strategies like Strangle, Straddle, and many others in different trading situations.

A trader may take long or short positions in both these options strategies. A long position means buying Calls and Puts. Short positions indicate writing options.

Traders use different options strategies to maximize trading profit. Options are financial trading tools used individually or in combinations. These options are used to formulate different options strategies. Strangle and Straddle are two different options strategies.

What are the Options?

As we discuss options strategies, it is best to look back into options basics. Options are financial derivative instruments. The value of the options is derived from the value of the underlying stock or indices if the options are index options. That is why these are called derivatives. The value of an option depends upon various scalable factors such as the Volatility of the Stock, the value of the underlying, the strike price, and days to expiry. Each of these factors directly affects the price of options.

Options are of two basic types, European and American. We in India deal only in European options. These options are represented by capital ‘E’. In India, the options are traded on the National Stock Exchange (NSE). Traders trade in two types of options, Call Options or CE and Put Options or PE. Here ‘E’ stands for a European type of option.

Call and Put

Traders can either buy or sell Call Options or CE and Put options or PE. An option buyer earns the right but not the obligation to buy or sell the underlying asset at a set price on or before a pre-determined date. A Call option buyer buys the option on the assumption that the underlying asset may go higher above a certain level. Similarly, a Put option buyer buys the options on the assumption that the underlying asset price may go down below a certain level.

In contrast to buying, option selling presents different opportunities. Options selling, also known as options writing, is a popular tool for hedging. Usually, options writing is just the opposite concept of option buying. Traders create opposite positions while writing options.

For example, a trader may write a call option if there is a possibility of the price of the underlying asset going down. Options strategies are used to hedge against volatility, time value, and directional hedging purposes.

Strategies

Options strategies are many in existence. Traders use options strategies that suit them and the market condition the most. Some of these strategies are popular strategies. Strategies like Straddle, Strangle, Butterfly, Iron Condor, Covered Call, and Put are popular options strategies. This article is entirely focused on the scope and trading techniques of straddle and strangle in options.

Options strategies help traders to minimize trading risks occurring from factors that affect options Greeks and undesired price fluctuations. Undesired price fluctuations give rise to unpredictable volatility occurring from unseen outside global and local factors influencing stock prices. A Straddle and a Strangle in options provide traders with tools to mitigate unforeseen volatility.

What is Volatility?

Volatility is the rate at which the price of security changes over time. Volatility also means the risk to which one’s investment in the stock market is exposed. Therefore, a trader can mitigate investment risk by controlling the exposure to price volatility.

Volatility has a normal tendency to return to its mean value after spikes over a period. One can rarely see that very high volatility persists over a long period. Options traders create positions to take advantage of volatility spikes when the trading situations demand that high volatility is imminent or wait for the high volatility to come down to normal and take advantage of the situation.

Types of Volatility

Volatility is of two types, Historical Volatility, and Implied Volatility or IV.

Historical Volatility

")

Volatility or historical volatility is a term associated with the price fluctuation of a stock over time, say a month, one year, etc. For the sake of standardization, it is referred to as the volatility of price over a year calculated on a daily basis. That is to say, we take the total price volatility of price over the last year and then divide the number by the total number of days traded to get the daily historical volatility measurement. Such volatility is a predictable and known quantity. A trader can adjust positions accordingly knowing the historical volatility.

Implied Volatility

Implied volatility indicates the future possible fluctuations of the price of the underlying. The pricing of options always considers implied volatility as an important parameter. Implied volatility, commonly referred to as iv, is the factor the price of an underlying is exposed to. The higher the iv, the higher the price of options and the higher the risk of trading.

With the employment of the right options strategy, a trader can minimize the investment risk and can make profits from high price fluctuations. When implied volatility is very high, options buyers profit from it and if implied volatility is on a continuously decreasing path, or if the implied volatility is low, the options sellers profit from it. The strangle and straddle strategies come into play in such situations.

We must keep in mind that implied volatility is a predictive number. Implied volatility represents a consensus of the market at a particular time. The number may not hold true all the time. That is why we need a cautious approach to tackle implied volatility. In the ongoing discussion, we will show the ways to tackle volatility through straddle and strangle options strategies.

Straddle and Strangle in Options

Straddle and strangle are two combinations of multiple options strategies. These strategies can be either short or long strategies or a combination of the two. We buy two options or short two opposing options (i.e. Put or Call) of the same strike prices or create other combinations. Let us discuss in detail how these two strategies work.

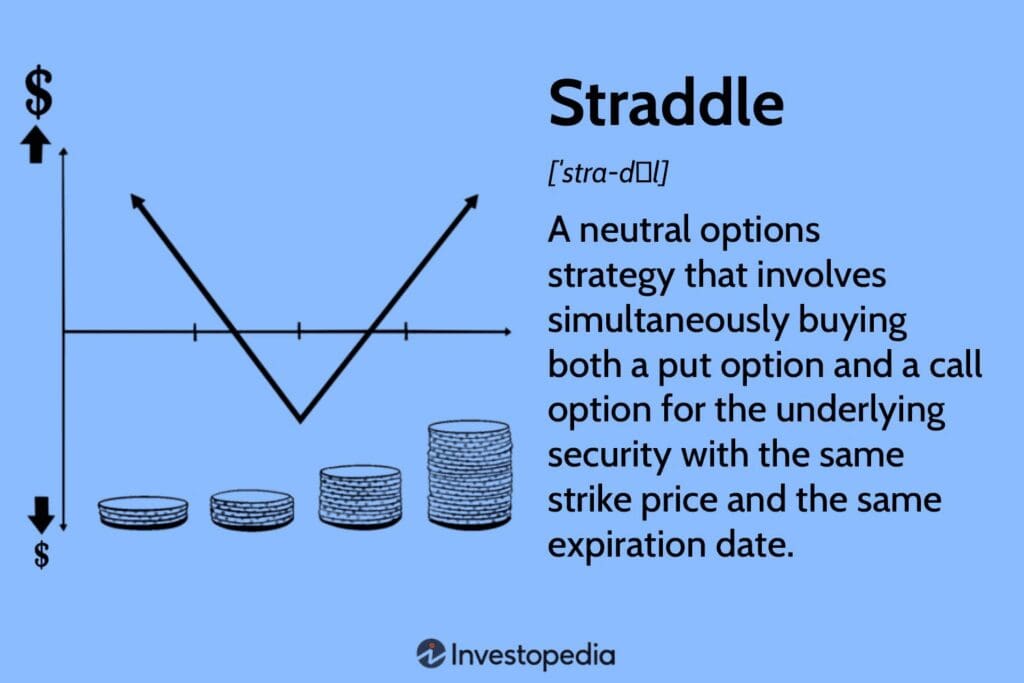

Straddle

Though the name is Straddle, it comprises Put and Call options in one single strategy. Straddle is a multileg options strategy. Traders use this strategy to mitigate trading risks.

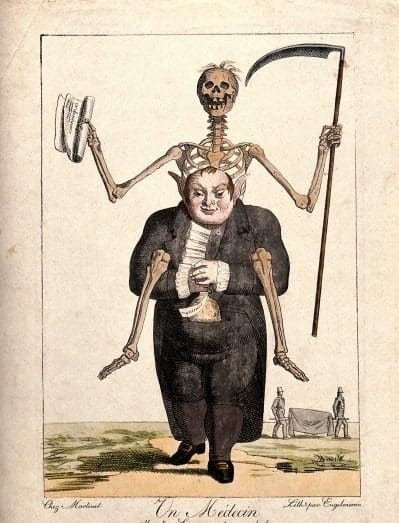

Straddle is a standard word in the English language which means sitting or standing with two legs apart or riding astride. The picture above contains the caricature of a doctor carrying a skeleton on his shoulder. The caricature is labelled as ‘ A doctor, straddled by a skeleton‘.

In the stock market glossary of terms, we use the meaning of straddle to identify a typical multileg options strategy.

Definition

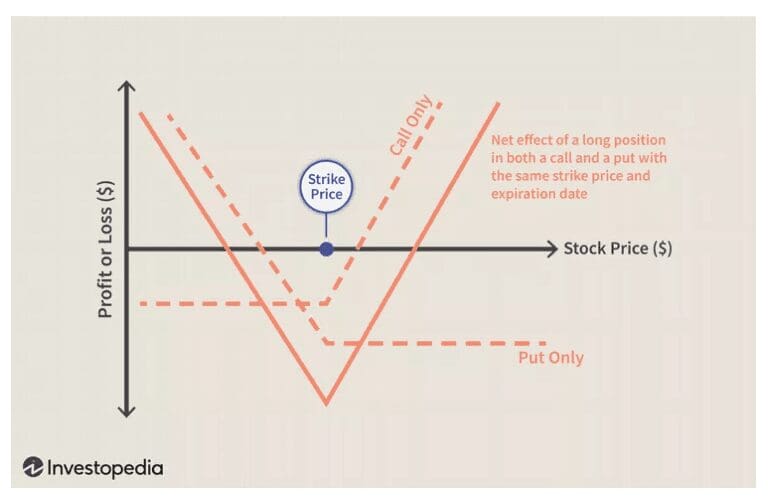

By definition, Straddle means creating an option strategy that involves buying or selling both Call and Put options of the same strike price that have the same expiration date. Straddle is essentially a direction-neutral strategy. The trader doesn’t take any directional view. Therefore, Straddle is a non-directional or direction neutral or neutral strategy.

A trader buys the Call and the Put of the ATM strike price simultaneously. The trader buys the Call and the Put of the 17500 strike price, of the same expiry to create a straddle position in Nifty, if the current price of Nifty is at 17490.

Characteristics of Straddle

The Straddle should have the following features.

- Positions should be in both Put and Call.

- Both options must have the same expiration date.

- Both options will be of the same strike price.

- Straddle is a multileg options strategy.

- The options strategy is non-directional.

- Both Call and Put are of the same stock or index.

- The straddle strategy implies that the stock or index is expected to complete the desired move within the expiry.

- The strategy is only profitable if the cumulative cost of Call and Put is less than the total selling price of the two options in the case of straddle buy.

Straddle is an options strategy. The trader takes a straddle position in options when the trader’s view is neutral. The trader believes that the underlying stock can go in either direction. The stock is poised to make a strong bull run or may start a sharp downtrend.

But the trader believes that the volatility is going to rise sharply. The price of options will also rise sharply if volatility rises fast. The trader doesn’t have any information or is not sure in which direction the price of the stock is going to move.

How to Construct a Straddle Option

In the stock market, such situations may occur before the start of a particular event. The event may be the annual budget declaration, the annual general meeting of the company, before parliamentary elections, or the before the declaration of the annual financial result. The stock price may react strongly based on the outcome of these events. Traders may create a straddle in options to take advantage of the sharp volatility rise before these events.

For example, say that stock A has good weightage on Nifty. Before the annual general meeting, there is general speculation that the company may take some important decisions that will be beneficial for the stockholders. A trader thinks that such speculation before the company AGM will create high volatility for the stock and options prices will increase for that.

Now, the price of the stock is Rs 2000 long before the AGM. The trader Buys a Call and a Put of the 2000 strike price. Both options have the same expiry. If the AGM is on 20th May, the trader must take the Call and Put options for the May expiry.

When to Create a Straddle

The trader expects to take advantage of the rise in options price due to the imminent rise in implied volatility. He/ She should create a short spread or sell both options just before the start of the event. The trader should sell both options when the expectation is very high, just before the event.

The trader expects that the volatility is going to rise when the AGM is near and the announcement is imminent. An increase in volatility will increase the price of both Call and Put of all the strikes, especially the strikes near the price of the underlying.

The volatility becomes maximum just before the AGM results are out. The trader expects to sell both Call and Put when their prices are maximum or near to it. It is not important in which direction the price of the stock will go. The trader makes a profit irrespective of the direction of the stock’s price. The only aspects the trader focuses on are timing and volatility.

Examples of Straddle Option Trading

The graphical presentation shows the straddle strategy application. A trader spends some money when the options are bought. Therefore, the trader can only make a profit when the combined price of the Put & Call goes above a certain price. The graph shows how the strategy makes a profit within the expiration date. We can explain that through an example.

Let us take the example of Infosys Ltd, a fundamentally strong stock. The current price of the stock is Rs. 1425.00. Let us take 1440 as the ATM price. Therefore the straddle of INFY is on 1440 strike price. The ATM call price is Rs 33 and the ATM put price is Rs 39. The upcoming date for the annual and Q4 result direction is April, 13th. The trader expects Infy to see high volatility in the stock before the 13th. April. Therefore, the trader is taking a position through the straddle strategy.

Cost Of straddle

The cost of straddle here is Rs (33+39 ) = Rs 72. The date of expiration of the options contract is 27-03-23. Rs 1440 is the ATM strike price and the combined cost of ATM options is Rs 72. Therefore, the cost of the premium paid is Rs 72 of the ATM strike of Infosys. This value suggests that the stock needs to move more than 5% on either side for the straddle to become profitable.

The value of stock price movement is reached through the following method. Rs 1440/ Rs 72 = 20. 100/20 = 5. Therefore a 5% move on either side will make the strategy profitable.

Trading range calculation

The trading range at which the trader will not lose all the money invested is Rs 1440 – Rs 72 = Rs 1368 to Rs 1440 + Rs 72 = Rs 1512. Within this range, if Infosys moves, the trader is expected to lose a little money. Beyond this trading range, which is below Rs 1368 and above Rs 1512, the straddle strategy is going to make money for the trader, if Infy ends up beyond this range at expiry.

Profitability Calculation

To calculate simply, we can add Rs 72 with both the Call and Put price to find the minimum price movement of either the Call or Put. Rs 72 + Rs 33 = Rs 105, which is the minimum threshold of the Call price. Therefore the Call price needs to go above Rs 105 to make it profitable alone if the Put price becomes 0. Similarly, the Put price needs to go above Rs 72 + Rs 39 = Rs 111 to make the Put profitable alone if the Call price becomes 0.

The conditions mentioned above suggest that, even if the trader does not sell the straddle during the pick volatility period, the stock has to move in one direction by more than 5% to make the straddle profitable, assuming that the other option becomes valueless during expiry.

The maximum loss will occur if the value of the underlying stock hovers around Rs 1440. In such a case, the price of both the Call and Put will finish worthless. The trader will lose all the money invested in such a case. Therefore, the stock must move by a great margin to make the straddle strategy successful.

The calculations above also suggested that unless the trader is not sure whether a high volatility period is imminent, the trader should not take the risk. The underlying stock must move a minimum of 5% to make the strategy clear the break-even value. A more than 5% move on either side is not a regular occurrence. Hence the time creating this strategy is important.

Advantages of Straddle Options

The straddle strategy presents manifold advantages.

- The strategy does not depend on any unpredictable price direction.

- The strategy earns from highly volatile situations.

- The trader can earn from price swings on either side.

- The strategy creates profit whether the stock price goes up or comes down by big margins.

- Before big events, when major mood swing affects the stock market traders are not sure of the outcome of the event, this strategy helps the traders to make good profit from unstable market conditions.

- Straddle helps to hedge against volatility.

- Straddle helps to mitigate risk from implied volatility and helps to make a profit from it.

Disadvantages of Straddle Options Trading

Though the straddle strategy has many advantages, it has some disadvantages too.

- The volatility needs to be very high if the trader wants to sell the options, that is, the trader wants to sell the straddle bought earlier before the expiration date.

- To make the strategy profitable, the underlying stock needs to move by more than the cost of the premium of ATM options paid by the trader.

- There is a need for the equity price to swing by a large amount to make Straddle profitable.

- The straddle strategy does not apply to all market conditions.

- The timing of the straddle strategy is very important. Therefore, a new trader may find it hard to profit from the straddle strategy.

- This strategy is especially suitable for stocks with low beta values.

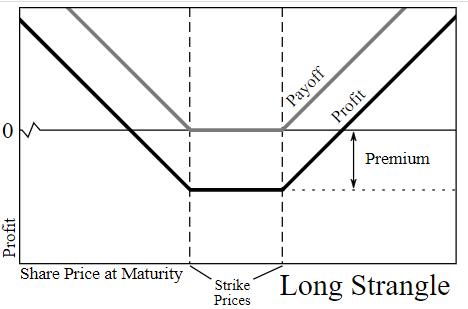

Strangle

Options trading is a form of investment that involves the buying or selling of contracts on underlying financial assets such as stocks, bonds, currencies, etc. A Strangle strategy in options trading involves the simultaneous purchase of both call and put options with different strike prices (the price at which an option can be executed). This type of trade usually consists of one long-term option and one short-term option; they are typically used when you believe there will be substantial movement in a particular asset but you’re not sure which direction it will move. The potential profit for this strategy lies in the volatility between time frames – if either contract is successful then profits can be made irrespective of market direction.

Definition

Contrary to the idea of the Straddle strategy, the Strangle strategy creates positions at two different strike prices, usually equidistant from the ATM strike price within the same expiry.

Say, Nifty is at 17490. The trader wants to create a Strangle in the next week’s expiry. Therefore, the trader buys a Call of 17600 and a Put of 17400 expiring next week, i.e. 20th April 2023. Here the trader creates a Strangle strategy expiring next week.

Therefore, it is a non-directional strategy. The trader employs this strategy whenever he/ she expects that a big swing in the stock is imminent but unsure of the direction of the movement.

The long-strangle strategy is only valid when there is a big swing about to happen in the stock in the near future. The strangle is very similar to the straddle strategy, but the strike prices are different. The Calls and Puts are of the same strike price for the straddle strategy, whereas the strike prices are different in strangle strategy.

How to Construct a Strangle Option

The Strangle options strategy requires the trader to buy the Call and Put of the same contract with the same expiry.

A trader buys this long-strangle strategy when the trader thinks there is going to be a big swing in price in the stock in the near future. But the price swing can take the stock go further up or a long way down. Hence, the trader buys a Put and a Call a little away from the current price under the same expiration date.

When to Create a Strangle

Usually, the Calls and Puts are bought at an equal distance from the ATM strike price. Say, for example, the Nifty 50 Index future is at 17500. Within a few days, the RBI is about to come forward with a new monetary policy. The trader sees here a big opportunity. The trader expects that Nifty is going to make a big jump either way.

Therefore, the trader buys a long call of 17700 and a long Put of 17300 of the options expiring in the next week, the week after the current week. So we can say that the trader has created a long strangle position to take advantage of the upcoming volatility in the index. The trader comes out of the strategy when implied volatility is at its peak and the index has made a definitive run in one way.

Though the diagram above shows the data of payoff at the expiry, a trader can come out of this strategy when the trader sees a good profit from selling both options.

Characteristics of Strangle

The Strangle strategy is somewhat similar to the straddle strategy. It should have the following features.

- Positions should be in both Put and Call.

- Both options must have the same expiration date.

- Both options will be of different strike prices.

- Usually, the Calls and Puts are placed at equidistant strike prices from the current ATM strike price.

- Strangle is a multileg options strategy.

- The options strategy is non-directional.

- Both Call and Put are of the same stock or index.

- The strangle strategy implies that the stock or index is expected to make a big jump in any trend direction within the expiry.

- The strategy is only profitable if the cumulative cost of Call and Put is less than the total selling price of the two options in the case of the long strangle strategy.

Strangle options strategy is very similar to the straddle strategy according to their features. The trader takes either of these strategies into options when the trader’s view is neutral. The trader believes that the underlying stock can make a big jump in price in any direction.

Examples of Strangle Option Trading

In the diagram above we can see two types of strangle strategies. We have used the long strangle strategy similar to the strategy used in straddle. These options strategies are for similar strategic trading. We use the short straddle or short strangle for different situations when volatility is coming down and may settle for a minimum in the near future.

We buy two opposite options expiring at the same period of the same contract. This is a pay-off diagram showing the profit and loss during the options expiry. The long strangle gives profit only after the stock has moved a certain distance after the strategy creation. Therefore, when we create a position, we must keep in mind the profit and loss diagram. The trader calculates the position even if the strangle options are sold during the expiry. But keeping in view the volatility or iv (implied volatility), the trader knows that the time to exit is when the volatility is at its peak or the iv has just started to come down. This is the reason, the trader creates such positions prior to an event.

Cost of the Strangle Strategy

Let us take the example of the strangle strategy made on Nifty, as we talked about earlier. The current price of Nifty Future is 17590. Hence, the ATM strike price is 17600. So we buy OTM options. We buy the Call 17800 and Put of 17400. The price of the Call is Rs. 25.15 and the Put is Rs 39.10. There the total cost of Strangle is (25.15+39.19) Rs. 64.25. The next week’s expiry is on 13.04.23. Hence Nifty must go above 17864 or go below 17335 for the Strangle to make a profit during the expiry. Here the trader only calculates the intrinsic value of options and the premium is out of calculation because all out-of-money (OTM) options become valueless during expiry.

The iv value is 21 now. If there is a case that the iv shoots high above before the expiry, the trader can exit from the strategy before expiration. At high volatility, the options price will increase and a high-profit opportunity will be open to the trader.

trading Range Calculation

The preferred trading range is above 17864 or below 17335 when the strategy makes a profit. The implied volatility adjustment is not there in this calculation. The strategy makes a maximum loss, i.e. Rs. 64.25 per lot of Nifty if the Nifty expires near 17600. Also, the loss will be the same if Nifty expires within 17400-17800.

Advantages of Strangle Options

The strangle options strategy offers less risk. The profit is also lesser unless the underlying stock makes big moves within the expiry. The other advantages are the same as explained in the Straddle options strategy.

Disadvantages of Strangle Options Trading

The disadvantages of Strangle options strategy are the same as the Straddle options strategy. The only added disadvantage is that the underlying stock needs to make bigger moves compared to straddle options for the strategy to make a profit.

Straddle Options Strategies

Following are the types of straddle options strategies the traders usually create in different situations.

Long Straddle

The long straddle is buying two opposing options of the same strike price expiring simultaneously. The strategy is suitable for the upcoming high volatility period.

Short Straddle

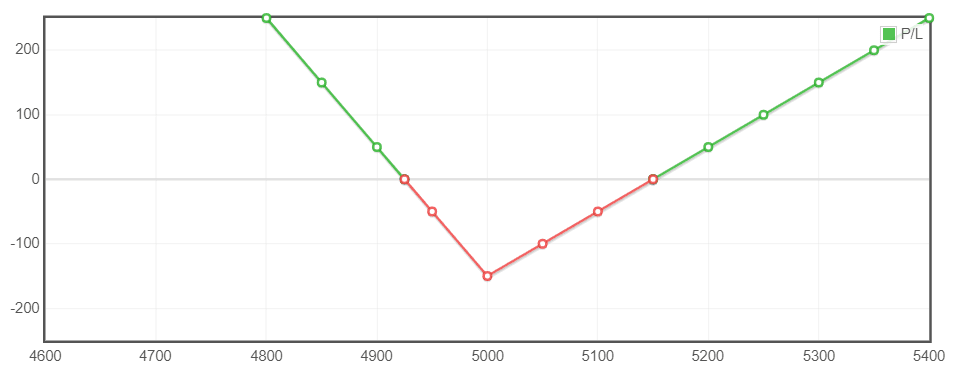

A short straddle is the selling of two opposing options of the same strike. The trader sells a Call and a Put of the same strike (usually the ATM strike price) of the same expiry. The trader expects the volatility will come down, the market will be stable and the expiry will be near the current strike price. In this case, the trader expects that the market will expire near the current price.

The pay-off diagram below shows that a trader creates an ATM short Straddle at a 5000 strike price. If the stock expires within 4900 to 5100, the trader is at profit, as shown by the green lines. The red line shows the loss-making zones. The maximum profit is at 5000. The cost of both options is Rs 50 each.

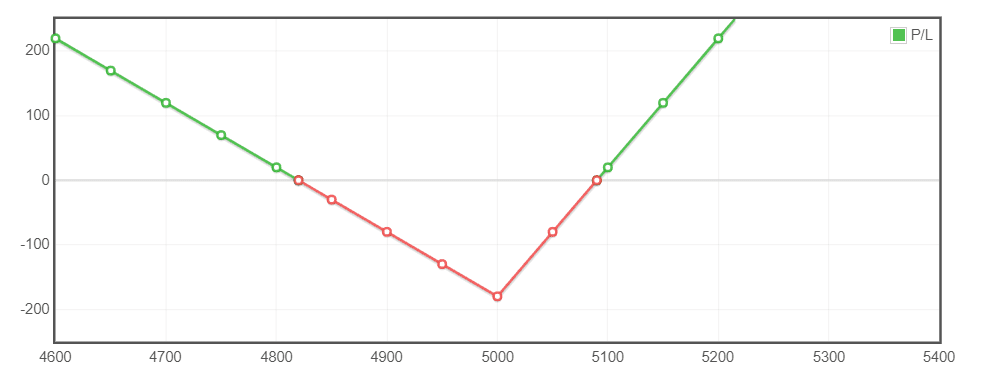

Strip

Strip involves purchasing two call options and a Put option of the same strike price. It is similar to adding a Call option to the long straddle strategy. This strategy has a bullish outlook.

The pay-off diagram above shows that the trader creates a long Strip position at the 5000 strike price. The trader buys two Calls and a Put at the 5000 strike price. If the stock expires between 4925 to 5150, the trader is at loss, as shown by the red lines. The green lines show the profit-making zones. Maximum profit is unlimited.

Strap

Opposite to the Strip strategy, Strap involves buying two Put options and one Call option of the same strike price under the same expiry. It has a bearish outlook.

The pay-off diagram above shows that the trader creates a long Strap position at the 5000 strike price. The trader buys one Call and two Puts at the 5000 strike price. If the stock expires between 4825 to 5075, the trader is at loss, as shown by the red lines. The green lines show the profit-making zones. Maximum profit is unlimited.

Similar to long Strip and Strap strategies, a trader also creates short Strip and Strap strategies when the trader expects the volatility to come down.

In addition, similar Strip and Strap strategies are possible if the trader takes a position in two different strike prices. These strategies are comparable to long and short strangles.

Strangle Options Strategies

Long Strangle

The long Strangle strategy is creating a strategy by buying one Call and one Put of different strike prices expiring at the same time.

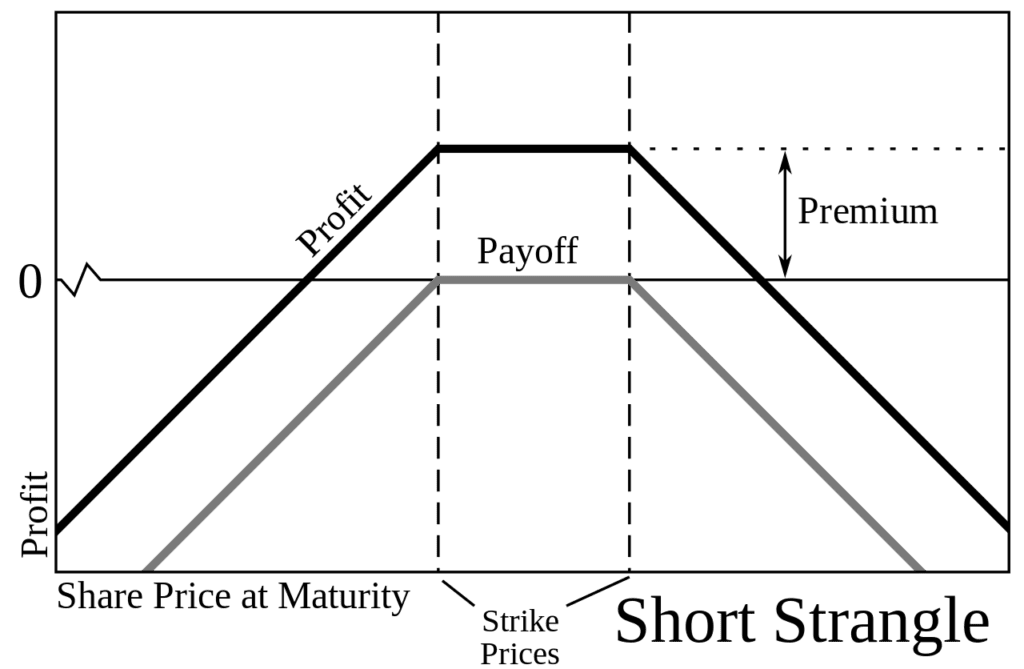

Short Strangle

The short Strangle strategy involves selling a Call option and a Put option of different strike prices expiring at the same time. The trader expects the volatility to come down and the stock to expire within the two strike prices.

The diagram of the short Strangle above shows that a trader sells a Call and a Put at different strike prices. The pay-off zone lies within the strike prices. The strategy gives profit if the derivative expires within these strike prices. The maximum profit is limited but the loss is unlimited.

Comparison between Straddle and Strangle Options

Straddle and strangle are two different but somewhat similar strategies. But there are differences also.

Difference between Straddle and Strangle Options Strategies

- A trader creates a straddle on a single strike price. But the strangle requires two different strike prices.

- Risk in Straddle is higher compared to Strangle strategy.

- A Straddle strategy costs more than a Strangle strategy.

- A Straddle strategy involves only ATM options. But a Strangle strategy requires only OTM (slightly OTM) options.

- The trader does not have any directional view of Straddle. But the Strangle trader assumes that the stock is going to move significantly in one direction but the trader wants protection against risk.

Similarities between Straddle and Strangle Option Strategies

- Both Straddle and Strangle in options involve buying or selling of similar numbers of opposing options, i.e. Calls and Puts.

- Both Calls and Puts expire on the same expiration date.

- Both of these strategies are risk-protected strategies.

- Straddle and Strangle are non-directional strategies.

Straddle vs Strangle – Which Option Strategy is Right for You?

When the trader expects the volatility is going to rise, it is best to take a long straddle or Strangle strategy. If there is an upcoming big event. it is best to go for a long Straddle.

When to use Straddle and Strangle Options Strategies?

A trader using the Straddle strategy has no directional bias. The trader only wants to gain from highly volatile situations.

When a trader uses Strangle strategy, the trader has a definite directional view but keeps protection on the opposite side. This strategy has a risk-protected directional view.

Advanced Strategies

Hedging Techniques Using Straddle and Strangle Options

Straddle strategies make good use of highly volatile situations. Straddle strategies help traders to hedge against volatility.

Vega

The effect of volatility in options is known as Vega which affects the price of options. A long Straddle or long Strangle gains from positive vega and vice-versa. By opting for long Strangle or Straddle strategies, a trader can hedge against rising volatility.

Delta

Besides Vega, other Greeks that affect the pricing of an option are Delta, Theta, Gamma, and Rho. The value of Delta primarily depends on the current stock price. By using Straddle which is a neutral directional strategy, we can hedge against changes in Delta to some extent, if the movement lies within a range. Strangle strategies help when the movement is unidirectional.

Theta

Hedging against Theta is mostly done through short Straddle or short Strangle strategies. With the falling Vega, the theta decay is easily manageable through such strategies. Theta decay shows the erosion in the value of options with the passage of time. By selling higher and buying lower the trader hedges against the value erosion of options.

Conclusion

The key concepts that we can summarize from this article are:

- Straddle and Strangle in options are two multi-legged, risk-mitigated options strategies.

- The strategies are non-directional strategies.

- The strategies help to hedge against volatility.

- Straddle and Strangle in options are similar strategies but used in different situations to fulfil different targets. But they have inherent differences too.

- Straddle is good before important events. Traders use Strangle strategies when a one-directional move is expected.

- Both strategies require good timing for entry and exit.

Final Thoughts and Tips for Options Trading

A trader should study the market situation before deciding on the type of strategies to take. If volatility is going to rise, the trader should create a strategy where vega is positive. In case volatility is coming down short strategies are more useful. The long/ short Strip and Strap strategies offset the non-directional nature of Straddle and Strangle options.

SIR, PLEASE MAKE THE VIDEO OF THE SAME TOPIC

Pranit, let me check for this. I already have a video on making money by selling straddles. Please search for it.