Introduction

In the world of options trading, Delta is the most commonly used Options Greek value. Delta measures the change in the option price for a unit change in the underlying asset. In this post, we will discuss Delta Neutral Strategy or Delta Hedging, which is a risk management technique that traders use to protect their portfolios against market movements.

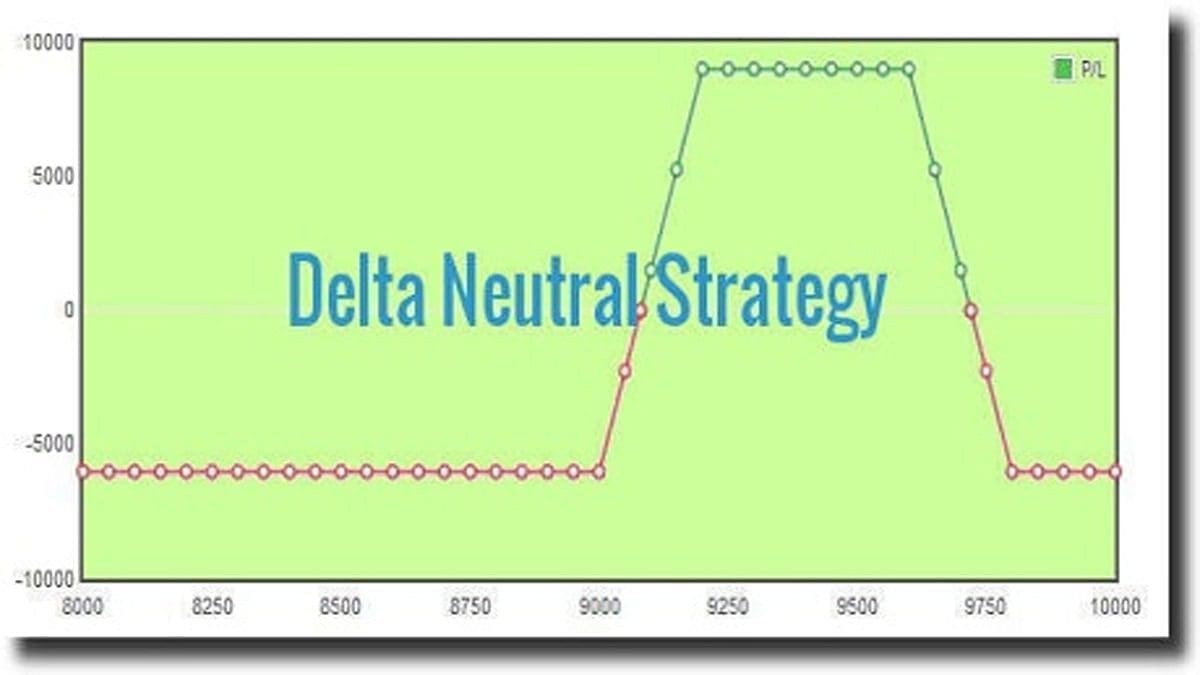

What is Delta Neutral Strategy for Hedging?

This is a strategy that involves balancing the Delta of an option with the underlying asset to create a position that is neutral to changes in the underlying asset price. In simpler terms, it is a strategy where the Delta of an option is offset by the Delta of the underlying asset to create a neutral position.

Delta Value Calculation

The Delta value of an option depends on the strike price and the time to expiration. For at-the-money (ATM) strikes, the sum of the absolute values of the call and put Delta is approximately 1. However, the Delta of the call option is positive, and the Delta of the put option is negative. By adding the Delta values of an ATM straddle, the total becomes nearly zero, which shows a Delta Neutral Strategy.

Delta Neutral Strategy Example

Suppose the Nifty index is trading at 9657, and the Delta value of the 9600 puts is 0.39, while the Delta value of the 9700 calls is -0.43. To create a Delta Hedging Strategy, we can short both the 9600 puts and the 9700 calls, assuming that the Nifty index will be range-bound and will not breach these levels. By adding the Delta values (0.39-0.43), we get a combined Delta value of -0.04, which is close to zero. If the Nifty index expires within this range, we can pocket the credit we received by taking a short position at those strike prices. You can check deltas and create option strategies using Options Oracle Pasi.

Benefits of Delta Neutral Hedging Strategy

A Delta Hedging Strategy can help traders to offset the effect of unpredictable variables like volatility and time decay. For example, if we buy 1 lot of SBI futures at 286 and simultaneously short 2 lots of 285 calls, the combined Delta value becomes zero, which creates a Delta Hedging position. This strategy can offset the time decay and give us a risk-free zone. Through dynamic Delta Hedging strategies like gamma scalping, we can also offset volatility.

FAQs on Delta Hedging

Yes, delta-neutral strategies can be very profitable in the Indian stock market. When implemented correctly, they offer traders a low-risk way to benefit from sudden and sharp directional price moves while keeping their risk exposure limited.

A classic example of a delta-neutral strategy would involve combining long positions on the call options with short positions on an equal number of puts with identical underlying securities/stocks and strike prices. This helps even out the risk of profit or loss determined by only one direction – either long or short.

By using delta-neutral approaches, traders gain profits through collecting both premium payments for options. They also earn capital gains from changing prices due to volatility in the Indian markets. A successful trader simply needs to have insight into when stock prices will move sharply resulting in higher premiums that could increase his considerations over time.

Delta Hedging Defi Strategy is an approach used by some cryptocurrency/Defi investors. This uses Options contracts as its primary hedging tool against fluctuations in both spot and futures markets for cryptocurrencies. It provides portfolio insulation against downside movements without completely detracting from upside potential gains.

Conclusion

Delta Neutral Strategy is a popular technique used by traders to manage their risk in options trading. By creating a neutral position using Delta and underlying assets, traders can protect their portfolios against market movements. Using Delta Hedging Strategy can help traders to achieve risk-free zones, which ultimately leads to a profitable trading experience.