The option pricing model gave us some tools which were named option Greeks. They are derived from the options pricing model. Since 1900, there have been several mathematical deductions by researchers to explain the rational pricing of options. But in 1973 Black, Scholes and Morten came up with the famous model, ‘The Black-Scholes Option Pricing Model’ which is the most rational form of option pricing and represents a close-to-real situation. They received Nobel Prize in Economics for this (Black passed away by then). For more information on Black-Scholes OPM kindly visit here.

What are the Option Greeks?

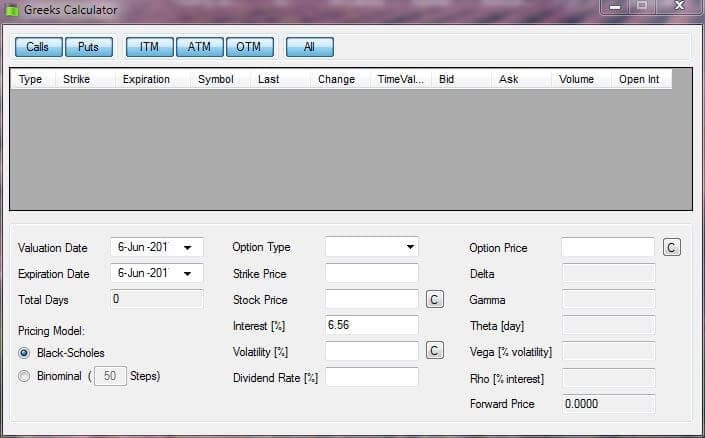

Greeks can be defined as the measurement of risk involved in taking a position in the option. The image shows a Greeks calculator using the Black-Scholes formula.

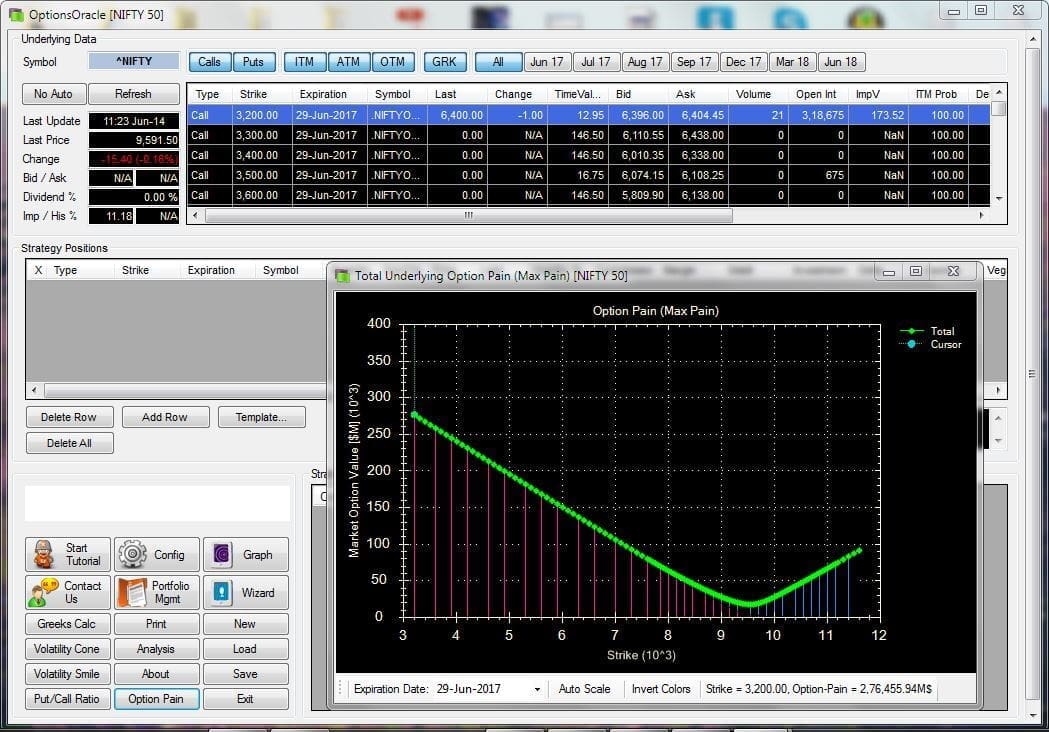

We have another post on Options Oracle Pasi. Here, are the usage details of Options Oracle. Before going live, one could have tested options strategies such as long strategies, short strategies, spreads, etc. It is a FREE of Cost service. You can download this Options Calculator at our Option Oracle Pasi page.

Types of Option Greeks

Options price depends on Volatility, time (days to expiry), risk-free interest rate, dividend besides stock price and strike price. Option Greeks are derivatives of the Black-Scholes model which define the risk involved. The main of the option Greeks are Delta, Gamma, Theta, Vega, and Rho. There are other Greeks as well which we can derive from the relation of these Greeks with the stock price. We will focus our discussion on these four first-order Greeks and one-second-order Greek.

Delta

Delta can be defined as the movement of the option price of a particular strike price caused by one unit price movement of the underlying stock. We denote Call deltas as positive while the delta of Puts as negative. The delta of options price is always less than 1. We consider the delta of stock future as 1. While preparing a strategy in options we primarily use delta to define the direction of the strategy. Direction refers to the bullish/ bearish stance taken while making the strategy.

We must always keep in mind that Delta of Calls and Puts of ATM (at the money) strike prices are near .5 (with a little shift). Use it as a thumb rule while calculating options price movement. Supposing 9650 is the ATM strike price of Nifty. Say the Call/ Put price of the ATM strike of nifty is Rs. 80 when nifty is at 9652. When can say that if nifty goes to 9672 from here, the Call/ Put price may increase/ decrease by Rs. 10 approximately (there are other factors which will change the price further).

Gamma

Gamma is the measure of the rate of change of Delta with respect to the price of underlying. Long options of both Call and Put have a positive correlation with Gamma and it is inverse in the case of a short position in options.

Gamma increases with the price and vice-versa. It is a second-order Greek as it we can derive it from the movement of the Delta. For a delta-neutral hedge strategy, a trader also looks to nullify Gamma so that the strategy remains effective for a longer range of price movement of the underlying.

Vega

It is another important constituent in option Greeks. It measures the change in options price with respect to the change in volatility of the underlying by 1%. At times option strategies depend heavily on volatility. It is important to consider Vega at such times. While taking a position in a straddle, we also consider it because the strategy is a comparatively aggressive strategy and high volatility affects it.

Theta

It measures the change in options price with respect to time. We can express it in annualized value in terms of days. We know all options contracts have a life which expires on the day of expiry. A weekly contract expires in 7 days (as in the case of weekly Banknifty options) or 30 days for a monthly option (as in Nifty). Though we can take position earlier, the contract will expire on the day of the weekly/monthly expiry.

The time value is maximum (implied in the options price) at the start of the contract and becomes zero on the day of expiry and the option price decreases accordingly. This phenomenon is nothing but time decay. Theta comes into play to measure the change in options price due to time decay. When one has a long position in options, he takes a short theta position and vice-versa. For a hedged position, you would want to have a theta-positive strategy to counter time decay.

Rho

Rho measures change in options value for a change in risk-free interest rate. It affects long-term strategies. But for the short term, option prices are not much affected by it. Therefore traders use it the least among option Greeks. It is expressed in terms of money with respect to changes in 1% of the risk-free interest rate.

How to Calculate Option Greeks?

We know, options are differently priced than the underlying. Options have some inherent characteristics which differentiate them from futures and stocks. Options are priced by keeping into account the market risk an investor faces when he takes the position. Pricing of options is done according to the famous Black -Scholes formula. Option calculator is a popular tool to calculate option Greeks for different strike prices.

There are different types of calculators available for calculating options prices. Some of them are offline and some are online calculators. Some of these calculators use the Black-Scholes option pricing formula, some use the Binomial option pricing model, some use the Monte Carlo simulations and some others used variations derived from these. But the Black -Scholes option pricing model is very popular as it gives close to a real-world situation when pricing options. In addition, they are more suitable for European types of options which we use in India (that is why we use CE or PE, E denotes European types of options). Also, this model has the advantage of fast calculation necessary for live market inputs.

Option Pricing Calculators

Option calculator using Black – Scholes pricing model is available in two formats. One is online and the other is offline, but both calculate options price and greeks. Traders use these models according to their convenience. Both types of models give similar results as both of them follow the Black -Scholes option pricing model.

Option Calculator in Zerodha

Zerodha has an online options calculator, the link of which we are giving here. We need to give various inputs to get the Greek value. The input variables are Stock price, Strike price, volatility, time (days to expiry), risk-free interest rate, and dividend. After one puts these variables into the Zerodha online option calculator, values of Greeks like Delta, Theta, Vega, Rho & Gamma come out below the calculator.

Options Oracle Pasi

There are many offline calculators as well. One popular offline calculator is Options Oracle Pasi. Developed for calculating options premium, this calculator also gives you values of Option Pain, Spread, Graphical representation of spread, Break even values and much other useful information.

FAQ

The five Greeks in options refer to Delta, Gamma, Theta, Vega and Rho. These terms define how an option’s price changes as the underlying stock moves or time passes. Delta measures an option’s sensitivity to the movements of the underlying security; Gamma tracks how quickly delta changes as a result of fluctuation in stock price; Theta refers to time decay and how value falls as expiration approaches; Vega looks at the IV or implied volatility of an option contract and finally, Rho records the change in cost when interest rates move.

Four Greeks exist for options – Delta, Gamma, Theta and Vega. Delta measures how sensitive an option is to movement on its underlying stocks while gamma tracks this shift rate. Theta represents time decay which is a decrease in value over time depending upon the approaching expiration date whilst vega looks at implied volatility such that higher volatilities will cause larger price swings within peak prices than those with low volatilities.

Option Greek or “the Greeks” are metrics used by professional traders who buy and sell options by measuring sensitivities against market conditions like stock prices & variations, implied volatility, time passage etc. They can employ these measurements as tools to assist trading strategies based on policy-formulating methods predicting gains or losses that offer protection from losses due to potential risks they entail.

Traders primarily use Greeks for Options Selling to measure sensitives involved during strategies employed in selling out contracts composed of derivatives instead of exercising them to purchase portfolio securities. Traders use Greeks to secure a profit on either a directional or non-directional basis using range-wide technicals calibrated by available data.

Conclusion

Option Greeks are vital tools for options traders to understand as they provide a way to accurately measure risk and reward factors associated with trading options. Traders who do not understand how to use option Greeks may underestimate or overestimate the risks and rewards involved in an option trade, leading to potentially disastrous results. By educating themselves on how these measures work, traders can increase their profits while keeping their investments safe. Option Greeks offer accurate assessments of an option’s position allowing investors to make informed decisions when carrying out trades, making it essential that all options traders educate themselves on these measures before engaging in any form of trading.