In order to analyze a company’s financial statement in fundamental analysis, you will find these terms again and again. Therefore, these basic financial terms should be clear to us. One thing is quite obvious standalone and consolidated are different from one another. So, at the end of the content, the ‘standalone vs consolidated’ concept will be clear.

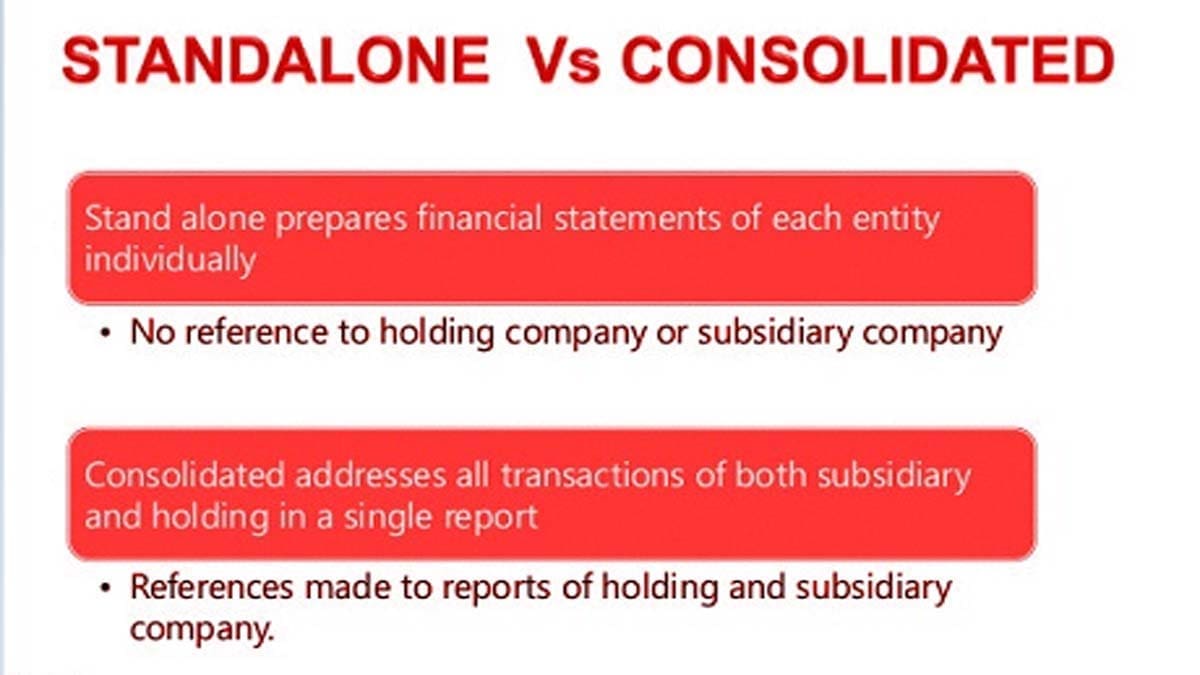

What is a Standalone Statement?

If a standalone statement connects with any ratio or profit, it means that the profit or ratio reflects the data of the parent company only. Standalone data is based on a single segment or division within a firm.

What is a Consolidated Statement?

Then the question is why the consolidated calculation is needed when we can read a company’s standalone result only for analysis. If a company has numerous subsidiaries then a consolidated financial statement is needed. Hence, consolidated results take into account the performance of the subsidiaries of a company.

Example of Using Both Standalone and Consolidated Financial Statements

Let’s take an example, suppose a company is XYZ and its subsidiary is XY. Both companies have their separate legal entity. Therefore, as per the law, both XYZ and XY can prepare their own financial statement separately. However, XY is the subsidiary of XYZ, it expresses XYZ can control the operating and financial decision of XY. So, XYZ in addition to preparing its own financial statement will also prepare a consolidated financial statement of XYZ and XY as a group.

Advantages and Disadvantages of Standalone vs Consolidated Data

One of the main advantages of getting both financial statements based on standalone and consolidated is investors can find out the health of not only the parent company but also its subsidiaries.

However, analyzing consolidated calculations is not as easy as analyzing standalone. As consolidated calculation requires lots of information, and data in comparison to standalone.

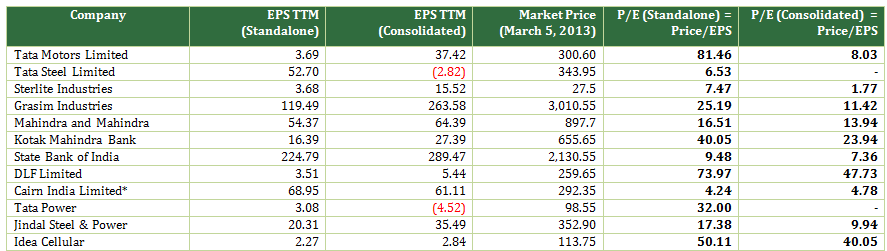

A Real-Life Example

The data shows standalone and consolidated results separately from each company listed above. As we have mentioned above standalone is based on the parent company’s data while the consolidated result includes all of the subsidiary company’s aggregate data.

FAQs on Standalone vs Consolidated Financial Statements

Standalone refers to the financials of an individual company, while consolidated financial statements consist of multiple businesses combined, resulting in one number representing the total net profit.

Standalone reports include only a single entity’s performance, whereas when companies consolidate their results, they are adding together all entities’ performances into one reportable figure for shareholders and other interested onlookers to review.

Consolidated financial statements combine separate but related legal entities such as parent-subsidiary corporations or different groups within a partnership or joint venture under the umbrella of one common corporate body; whilst combining involves merging similar items from various legal entities that continue to be distinguished from each other despite this merging process on paper not in practice.

Standalone financials show how well a single business unit has performed by itself without taking into consideration any affiliated firms’ contributions or effects – either positively or negatively – on its bottom lines figures such as revenue streams and profits advanced levels of efficiency etc.

Conclusion

In conclusion, in the case of analyzing a company’s data accurately, both standalone and consolidated results are important. Investors can get an aggregate overview of the company’s growth, profitability, and debt amount from it.