Are you someone who is confused between debt funds and fixed deposits? Do you want to know which one is better for you? If yes, then you are in the right place. In this article, we will discuss the differences between debt funds vs FD or fixed deposits, and help you decide which one you should choose based on your financial goals.

Section 1: What are Debt Funds?

Debt funds are mutual funds that invest in fixed-income securities such as corporate bonds, government bonds, and money market instruments. They are called debt funds because they lend money to the issuer of the securities and earn interest income in return. Debt funds are managed by professional fund managers who invest in a diversified portfolio of debt securities, with the aim of generating regular income for investors.

Types of Debt Funds

- Short-term Debt Funds: These funds invest in debt securities with a maturity period of fewer than 3 years. They are less risky than long-term debt funds, but they also offer lower returns.

- Long-term Debt Funds: These funds invest in debt securities with a maturity period of more than 3 years. They offer higher returns than short-term debt funds, but they are also riskier.

- Corporate Bond Funds: These funds invest in corporate bonds issued by companies with a credit rating of AA and above. They offer higher returns than government bond funds, but they are riskier.

Advantages of Debt Funds

- Diversification: Debt funds invest in a diversified portfolio of debt securities, which helps to reduce the risk of the portfolio.

- Professional Management: Professional fund managers who have expertise in the field of fixed-income securities manage debt funds.

- Liquidity: Debt funds offer high liquidity as investors can redeem their units at any time.

- Tax Benefits: Debt funds offer tax benefits to investors who hold their units for more than 3 years. The gains made by the investors are taxed at a lower rate than fixed deposits.

Section 2: What is a Fixed Deposit?

Fixed Deposit or FD is a popular investment option offered by banks and other financial institutions. In a fixed deposit, the investor deposits a certain amount of money with the bank for a fixed period, ranging from 7 days to 10 years, and earns a fixed rate of interest on the deposit.

Advantages of Fixed Deposits

- Guaranteed Returns: Fixed deposits offer guaranteed returns on the invested amount, irrespective of market fluctuations.

- Low Risk: Fixed deposits are considered a low-risk investment option as the returns are guaranteed.

- Ease of Investment: Fixed deposits can be easily opened by visiting the bank or through online banking.

- No Market Risk: Fixed deposits do not expose the investor to market risk, unlike equity investments.

Section 3: Debt Funds vs FD – Understanding The Key Differences

Debt funds and fixed deposits are both popular investment options in India. While both offer the opportunity to earn interest income on investments, they differ significantly in terms of returns, risk, and liquidity.

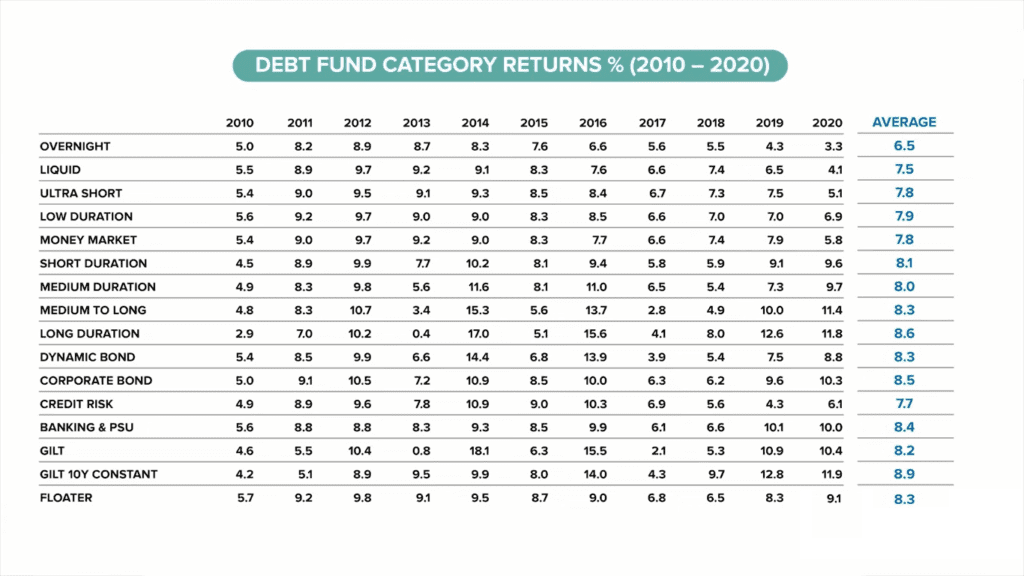

Returns: Debt funds offer higher returns than fixed deposits, especially over the long term. The average return on fixed deposits is around 6-7%, while the average return on debt funds is around 9-10%. However, it is important to note that debt funds are subject to market risks and the returns may vary depending on the performance of the underlying securities.

Risk: Fixed deposits are considered a low-risk investment option as the returns are guaranteed. On the other hand, debt funds are subject to market risks and the value of the investment may fluctuate depending on the performance of the underlying securities. However, debt funds also offer the advantage of diversification, which helps to reduce the risk of the portfolio.

Liquidity: Fixed deposits have a fixed lock-in period, which ranges from 7 days to 10 years, depending on the bank. Once the lock-in period is over, the investor can withdraw the funds, but they may have to pay a penalty for premature withdrawal. On the other hand, debt funds offer high liquidity as investors can redeem their units at any time.

Taxation: The gains made on fixed deposits are taxed as per the income tax slab of the investor, which can be as high as 30%. On the other hand, debt funds offer tax benefits to investors who hold their units for more than 3 years. Investors pay taxes on the gains at a lower rate than fixed deposits.

Section 4: How to Choose Between Debt Funds and Fixed Deposits (FD)?

Choosing between debt funds and fixed deposits can be a difficult decision, especially for investors who are new to investing. Here are some factors that investors should consider while making a decision:

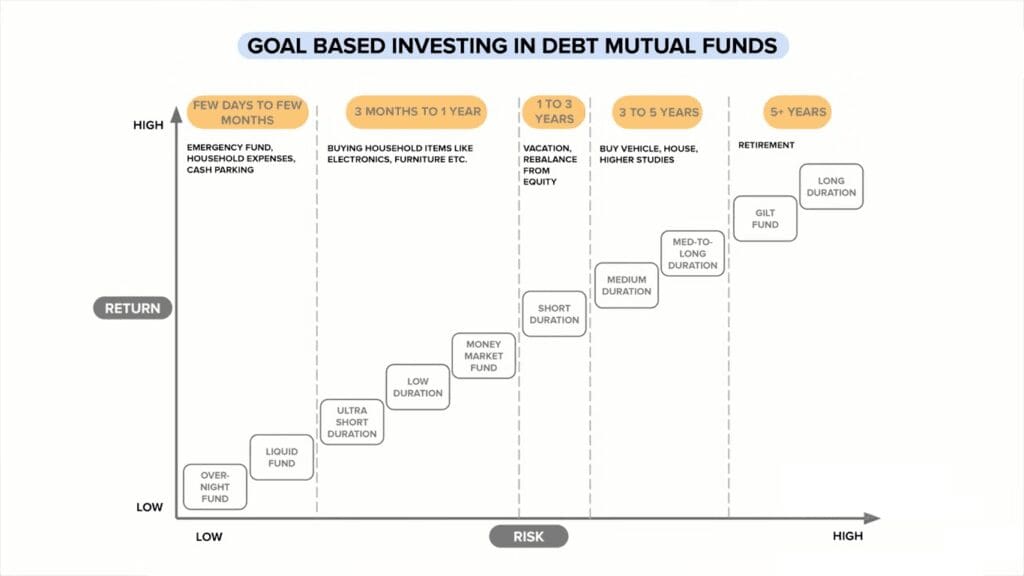

Investment Horizon: Debt funds are suitable for investors with a medium to long-term investment horizon, while fixed deposits are suitable for investors with a short to the medium-term investment horizon.

Risk Appetite: Debt funds are suitable for investors who are willing to take moderate risks for higher returns, while fixed deposits are suitable for investors who are risk-averse and prefer guaranteed returns.

Tax Implications: Debt funds offer tax benefits to investors who hold their units for more than 3 years. On the other hand for fixed deposits, investors need to pay tax at a higher rate than debt funds.

Liquidity: Debt funds offer high liquidity, while fixed deposits have a fixed lock-in period.

Investment Amount: Fixed deposits have a minimum investment amount, which is usually Rs. 1000, while debt funds have no minimum investment amount.

Debt Mutual Funds That Are Likely To Beat Fixed Deposit Returns

Here are three debt mutual funds that are likely to beat fixed deposit returns:

- ICICI Prudential Short-Term Fund

- ICICI Prudential Regular Savings Fund

- ICICI Prudential Corporate Bond Fund

Section 5: FAQs on Debt Funds vs FD

It depends on your financial goals. If you are looking for guaranteed returns with low risk, then FD is a better option. However, if you are looking for higher returns with moderate risk, then debt funds may be a better option.

Debt funds offer higher returns than fixed deposits, especially over the long term. They also offer tax benefits and high liquidity, which is not available with fixed deposits. Debt funds are clear winners if we compare debt funds vs FD.

Yes, it is a good time to invest in debt funds, especially short-term debt funds, and corporate bond funds, as they offer higher returns than fixed deposits.

Yes, debt funds can give negative returns if the credit rating of the underlying securities is downgraded. However, the risk can be mitigated by investing in a diversified portfolio of debt securities.

Section 6: Conclusion

In conclusion, debt funds and fixed deposits are both popular investment options in India. While both offer the opportunity to earn interest income on investments, they differ significantly in terms of returns, risk, and liquidity. Investors should consider their investment horizon, risk appetite, tax implications, liquidity, and investment amount while making a decision. While fixed deposits are suitable for investors who prefer guaranteed returns with low risk, debt funds are suitable for investors who are willing to take moderate risks for higher returns. However, investors should also remember that debt funds are subject to market risks and the returns may vary depending on the performance of the underlying securities. Therefore, it is important to invest in a diversified portfolio of debt securities to mitigate the risk.