With the Anchored VWAP indicator, the trader can associate VWAP computations with a particular price bar. Traders can use it to locate regions of support and resistance on the chart. Also, like the conventional VWAP, combines price and volume in a weighted average. Traditional VWAP calculations, on the other hand, always begin with the first bar of the day and terminate with the last bar. In certain circumstances, a chartist would prefer to evaluate the VWAP line using a less arbitrary starting point and to be able to prolong that VWAP line past the close of trading.

Anchored VWAP: What is it?

Here we use a user-selected starting point to display the volume-weighted average price for a given time period using AVWAP. In other words, Anchored VWAP displays an asset’s price adjusted for its volume starting at any selected point on the chart. This is an effective tool since it visualizes each price level as a smooth line. It also accounts for the volume of shares traded at each level.

Anchored VWAP makes it simple to determine whether the bulls or bears have been in control since a very particular time period by allowing you to pick the price bar where calculations begin. A change in market psychology, such as a notable high or low, earnings, news, or other announcements, is typically what we use as the opening price bar what we use. The price and volume information following that important occurrence is used to chart the AVWAP line.

A Little Historical Context

The late physicist and technical analyst, Paul Levine, created the Anchored VWAP tool between 1995 and 1997. He was working on the Market Interpretation/Data Analysis System (MIDAS). In the 1980s, professional trader Kevin Haggerty employed volume-weighted average price curves to determine the direction of a position. Levine created this system. Few people and organizations still promote the story of Anchored Volume Weighted Average Price even today. They are Brian Shannon, Zach Hurwitz, and the CMT Association, which has done a tremendous job of mainstreaming it.

Calculation of the Anchored VWAP

You can use the same formula to calculate the standard VWAP as well as the Anchored VWAP. The bars used in the computations are the only thing that differs.

Traditionally, we use the first bar of the day and the last bar of the day to calculate VWAP. Traditional traders use VWAP only for intraday charts because it only uses data from one trading day.

When using Anchored VWAP, the chartist selects the initial bar to use in the calculation. This is “anchoring” the indicator to that bar. The final bar is always the most recent bar that is available. The use of Anchored Volume Weighted Average Price is not restricted to intraday charts because of the more adaptable starting and ending locations. For additional information on the standard method used to determine both VWAP and Anchored VWAP, please check our article on VWAP.

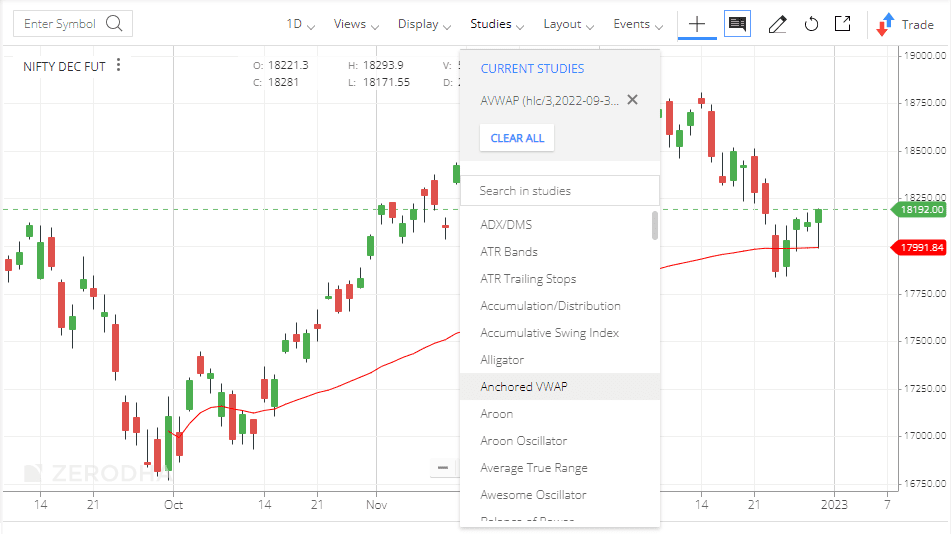

AVWAP Application to a Chart

The Zerodha Kite Chart Settings panel allows you to add this overlay. I prefer ChartIQ version 7 to draw this indicator.

You need to select a starting date and time when you add Anchored VWAP to your chart. But you can simply change these to suit your technical analysis requirements. Although Zerodha Kite offers a faster alternative, you can manually amend the Anchor Date and Anchor Time fields by changing the parameters on the chart. You can also long press and drag the indicator to the bar where you wish to start your Anchored VWAP overlay. You need to mark the correct Anchor Date and Anchor Time.

- As shown below, choose Anchored VWAP from the list of drawing tools on the chart’s indicators panel.

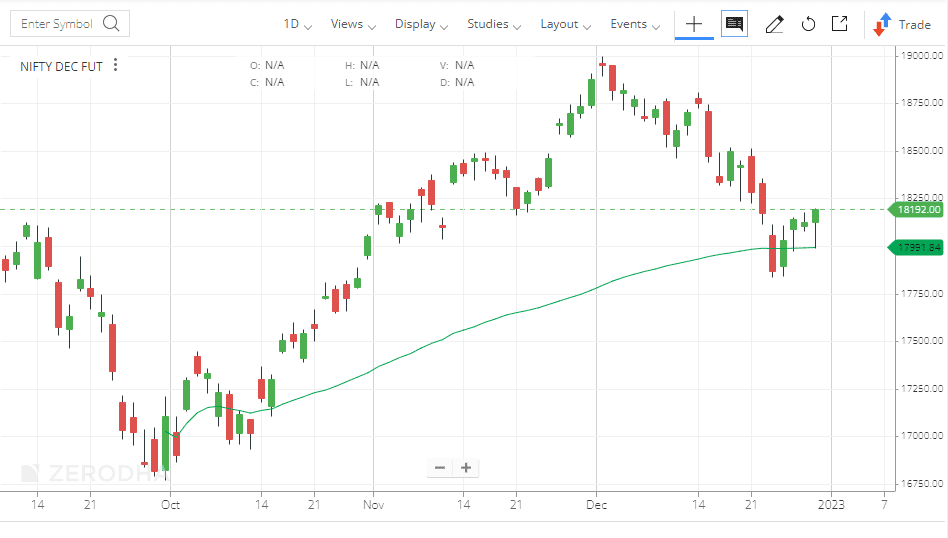

- Select the starting point for your computation by clicking on the chart. Here I have selected 30/09/2022 as the anchor date in the hourly chart as this was a major low. I have also made the colour green as this can be my major support. The chart will show the volume-weighted average price curve as shown in the illustration below.

By right-clicking on the line and choosing the necessary parameters in Settings, you can also alter the colour of the Anchored VWAP and add standard deviations to it.

Using the Anchored VWAP to Interpret

The Anchored VWAP overlay, like conventional VWAP, can validate trends. It can also spot regions of support and resistance on the chart. The benefit of utilizing AVWAP is that you can choose the starting point so that you can only see pertinent data on your chart.

Typically, the chartist selects a specific event – a notable high or low, an earnings report, a gap, etc as the starting price bar for the overlay. The price action before these occurrences, which does not represent the same market psychology, should be omitted from the calculations. This is because they typically signal a change in the market’s psychology.

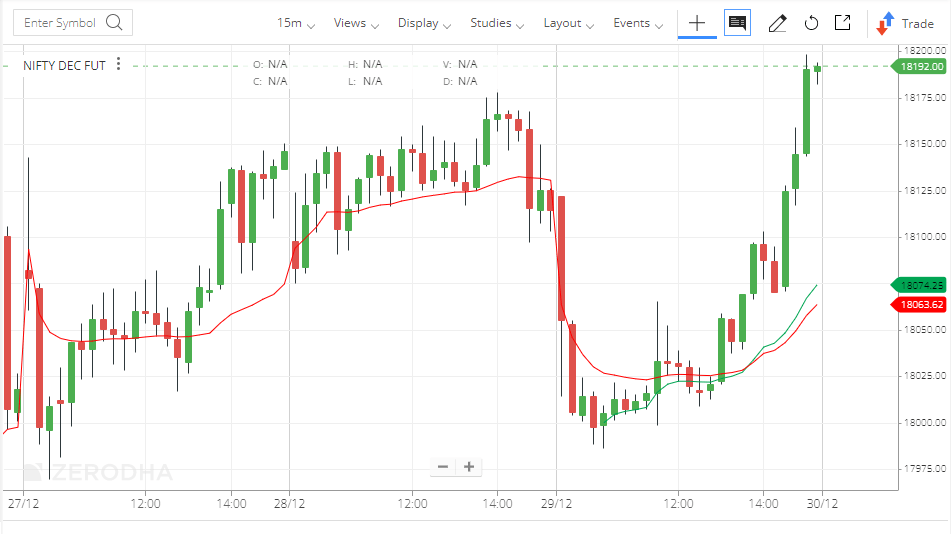

For instance, the VWAP line (in red) in the Nifty futures 15-minute chart below is based on the opening bar. Here, the Anchored VWAP line (in green) is set at the morning low made at 10:15 AM today. The red VWAP line includes information for both the significant fall in price during the first 60 minutes of trading and the steep increase to the day’s high, resulting in a VWAP line that does not accurately depict the price movement at midday. The green Anchored VWAP line more properly depicts the noon market psychology because it only includes data after reaching the bottom. Check the market rally once the AVWAP (green line) crossed above the normal VWAP (red line) here.

On a single chart, several anchored VWAP lines can be utilized, each one anchored at a different starting point. A very potent point of support or resistance can come out by the convergence of numerous Anchored VWAP lines.

AVWAP versus VWAP

You can plot the VWAP and AVWAP together on a single chart to analyze market trends and spot trade setups. I have already shown you the example in the last image.

From the information provided above, it is clear that AVWAP is flexible. We generally do not use it for intraday trading, whereas we utilize VWAP to identify intraday patterns. Plotting both, nevertheless, can make it easier for you to trade effectively.

FAQ

Anchored VWAP (Volume Weighted Average Price) is a technical trading indicator that plots intraday price data points based on volume. Traders can use it to identify a stock’s trend and analyze trading patterns for better decision-making.

While Volume-Weighted Average Price (VWAP) only takes into account historical daily prices, Anchored VWAP allows traders to adjust for intra-day factors such as news announcements or unexpected economic events by anchoring the start point of calculation at any given time in anticipation of price movements.

Yes, Zerodha offers an assortment of advanced charting tools including Anchored Volume Weighted Average Price (AnchoredVWAP). This tool helps investors analyse up to five past sessions simultaneously with different drawing styles and customisable settings to improve strategy performance.

Intraday Volume-Weighted Average Prices (vwap) are calculated using end-of-day values from one period whereas Moving vwap uses two previous periods’ values thus providing more accurate estimates. Notably, Intraday vwap does not take into consideration open positions resulting in less reliable analyses whereas Moving VWAPs can also factor in these elements thus providing additional insight when analyzing trends over multiple consecutive days.

Conclusion

In terms of setting support and resistance levels, anchored VWAP offers all the same advantages as regular VWAP. Now with the added benefit that you may specify the precise duration to conduct your research. You can remove price activity that was influenced by different market psychology by beginning VWAP calculations at the time of a critical turning point.

Traders should use the Anchored VWAP overlay with other technical indicators and research methods, as they should with all technical indicators.