Introduction: Why Every New Investor Should Care About Compounding

If you’ve just started your investing journey in India and are wondering how to turn a modest monthly SIP into a substantial corpus, you’re not alone. Many beginners are confused by the term and example of power of compounding, hearing it in YouTube videos, AMFI campaigns, and even from relatives bragging about their retirement funds. But what does it really mean? And more importantly, how can it help you build wealth even if you start with small amounts?

The power of compounding refers to the process where your investment earns returns, and then those returns themselves start earning more returns. Over time, this snowballs into a massive corpus, even if your monthly contributions are small. In essence, compounding turns time into money — and lots of it.

As someone who has been actively investing and educating Indian traders and investors for over 15 years, I’ve seen firsthand how this seemingly boring concept quietly creates crorepatis. Whether it’s a student starting a ₹500 SIP or a salaried employee stashing away ₹5,000 every month, those who understand compounding—and start early—often end up with enviable wealth.

This blog will demystify compounding for you, backed by real Indian examples, mutual fund data, relatable stories, and actionable strategies. You’ll discover how a ₹1,000 investment can grow into lakhs and why waiting even five years to start could cost you crores.

Let’s break it down step by step so that by the end of this guide, you’ll not just understand the power of compounding example — you’ll know exactly how to use it.

What Is the Power of Compounding in Simple Terms?

The answer is: The power of compounding is when your earnings generate more earnings over time, leading to exponential growth of your investment.

Think of it like this: You plant a mango seed (initial investment). It grows into a tree (your returns). That tree gives you more seeds (reinvested returns), which grow into more trees. Over years, your small seed becomes a massive orchard.

Let’s Look at a Simple Indian Example

- Year 1: You invest ₹1,000 at 10% interest → You earn ₹100 → Total: ₹1,100

- Year 2: 10% on ₹1,100 → ₹110 → Total: ₹1,210

- Year 3: 10% on ₹1,210 → ₹121 → Total: ₹1,331

This keeps growing exponentially—not linearly. And that’s the magic.

Real-World Example: Reliance Growth Fund

Had you invested ₹1,00,000 in Reliance Growth Fund in 1995, today you’d have more than ₹1 crore — that’s over 100x growth due to long-term compounding in equities. This fund is a textbook example of how compounding rewards patient investors.

Key Takeaway

The earlier you start and the longer you stay invested, the more powerful compounding becomes. It’s not about how much you invest, but how long you let it grow.

Why Time is the Greatest Multiplier — Not Capital

The answer is: Compounding needs time more than large investments. A small amount invested early beats large amounts invested late.

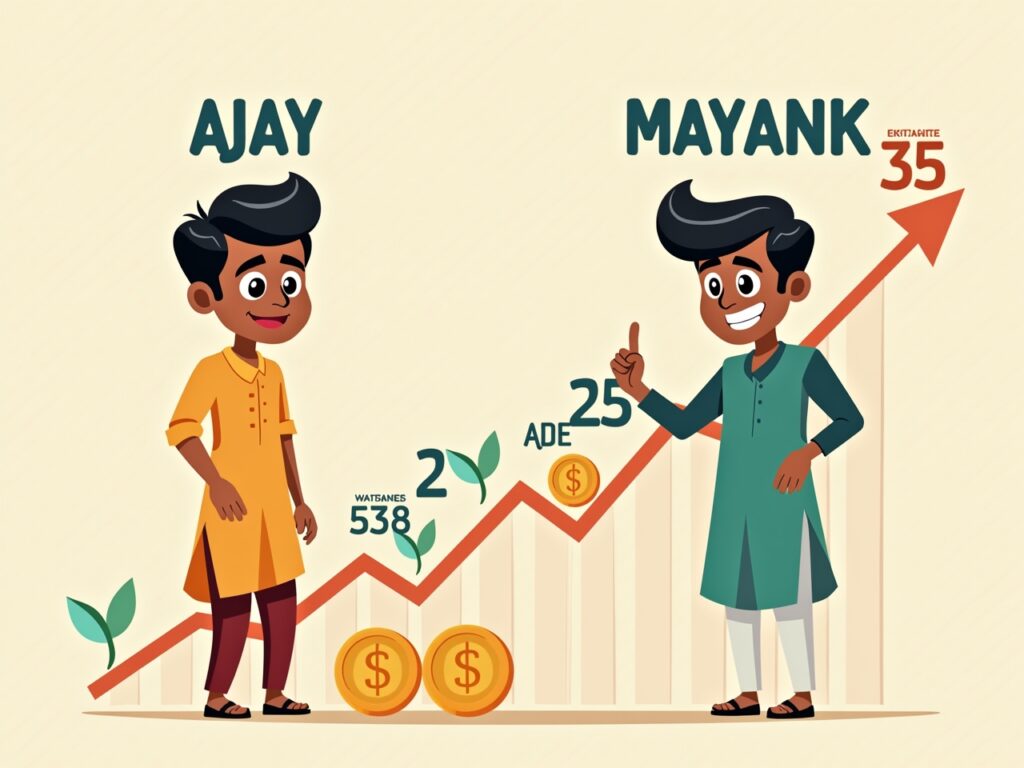

The Tale of Two Investors: Ajay vs. Mayank

From Kotak Securities’ popular video:

- Ajay started investing ₹5,000/month at age 25 and stopped at 35 (10 years total).

- Mayank started at 35 and continued ₹5,000/month till age 60 (25 years).

At retirement, Ajay had ₹1.12 crore, while Mayank had just ₹76 lakh — despite investing 2.5x more money.

That’s the power of starting early. Mayank gave compounding less time.

Hypothetical: The Magic Penny

If a penny doubles every day for 30 days, by day 30, you have over ₹40 crore. That’s exponential growth in action. For the first 20 days, it still looks like “not much is happening.” Then — boom.

Summary Table: Small Starts vs. Late Starts

| Investor | Start Age | Monthly SIP | Duration | Final Corpus (10% return) |

|---|---|---|---|---|

| Asha | 25 | ₹2,000 | 35 yrs | ₹94.3 lakh |

| Ravi | 35 | ₹5,000 | 25 yrs | ₹82.2 lakh |

Time in the market always beats timing the market.

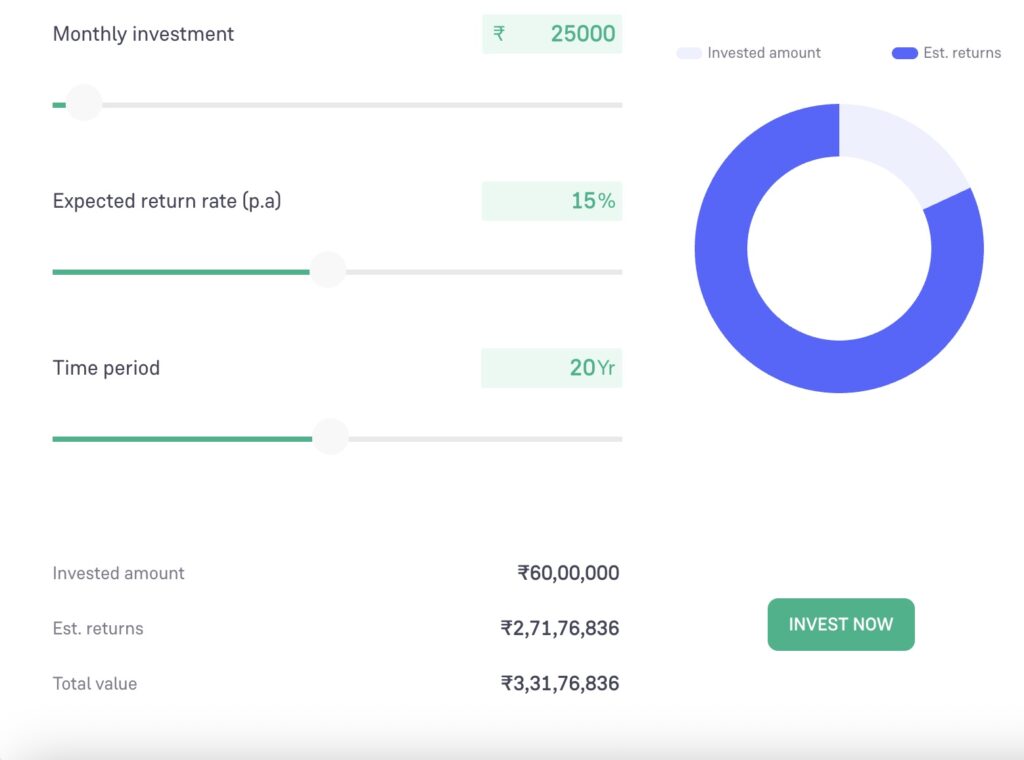

How SIPs Help You Harness Compounding in India

The answer is: SIPs (Systematic Investment Plans) allow you to consistently invest and reinvest, making them ideal for compounding returns.

Why SIPs Are a Beginner’s Best Friend

- Automates investing, removing emotions

- Rupee cost averaging helps during market ups and downs

- Reinvestment of gains happens by default

- Ideal for salaried individuals and students

Example: Groww User’s Real Testimonial

“I started with ₹1,500 SIP in ICICI Prudential Balanced Fund back in 2013. I never skipped a month. As of 2025, my investment of ₹2.1 lakh is now worth ₹4.7 lakh. I didn’t even notice the growth — it just happened!” — Ritu, Mumbai

Pro Tip: Choose Growth Over Dividend

When investing in mutual funds for compounding, select Growth option, not Dividend Payout. Growth keeps reinvesting your profits, maximizing compounding.

Trusted Indian Funds for Long-Term SIPs

- Axis Bluechip Fund

- Mirae Asset Large Cap Fund

- Parag Parikh Flexi Cap Fund

Always consult a SEBI-registered advisor before investing.

A disciplined ₹500 SIP today is better than a ₹50,000 lump sum you may never invest.

What’s the Real Difference Between Simple Interest and Compound Interest?

The answer is: Simple interest grows linearly; compound interest grows exponentially.

Simple Math:

- Simple Interest (SI) = P × R × T / 100

- Compound Interest (CI) = P × (1 + R/100)^T – P

Let’s compare:

| Initial Amount | Interest Rate | Period | Simple Interest | Compound Value |

|---|---|---|---|---|

| ₹1,00,000 | 10% p.a. | 20 yrs | ₹2,00,000 | ₹6,72,750 |

You earn ₹4.7 lakh more just by compounding!

Common Misconception

Many Indians think putting money in an FD at 6% for 5 years is “safe and growing.” But the real growth comes only when the interest earns interest.

Pro Tip: Compounding Frequency Matters

- Annual: Once per year

- Quarterly: Every 3 months

- Monthly: Best for SIPs

More frequent compounding = faster wealth building.

Risks and Realities: When Compounding Doesn’t Work as Expected

The answer is: Compounding only works if you give it enough time and avoid withdrawing early or skipping contributions.

Real Mistakes People Make

- Stopping SIPs during market downturns

- Redeeming early to fund short-term goals

- Skipping months, breaking the compounding chain

- Choosing dividend options over growth

A Reddit User’s Regret Story

“I paused my SIPs during COVID in 2020 out of fear. I later realized that the market bounce-back doubled my fund net asset value (NAV) in 1.5 years. Had I continued, I’d be ₹2.5 lakh richer.”

Other Factors That Can Erode Compounding

- High fund expense ratios

- Tax inefficiency (short-term capital gains)

- Overtrading in direct equities

Compounding is not magic — it’s science + discipline.

How to Start Compounding Today — Even If You’re a Total Beginner

The answer is: Start small, start early, and stay consistent. You don’t need to be rich to build wealth with compounding.

Step-by-Step Action Plan

- Choose a trusted platform like Zerodha Coin, Groww, or Kuvera

- Set up a ₹500–₹1,000 monthly SIP in a diversified mutual fund

- Select the Growth option

- Automate it via ECS

- Track it yearly — not monthly

- Avoid stopping unless truly necessary

Suggested Funds for First-Time Investors

| Fund Name | Risk | Ideal Time Horizon |

|---|---|---|

| UTI Nifty Index Fund | Low | 10+ years |

| Axis Bluechip Fund | Moderate | 5+ years |

| Parag Parikh Flexi Cap | Moderate | 7+ years |

A Real Story: My Own Start in 2009

Back in 2009, I started a ₹2,000 SIP in HDFC Top 200 Fund. I stayed invested for 12 years. That single SIP is now worth ₹6.1 lakh, even though I only invested ₹2.9 lakh. I never traded, just held tight. That’s what compounding does when you let it run.

If you can’t invest ₹1,000/month, start with ₹500. But start today.

Conclusion: Embrace the Eighth Wonder of the World

The truth is: You don’t need market timing skills or big capital to become wealthy — you need time, consistency, and the power of compounding.

Whether you’re 22 or 42, the sooner you begin, the more your money will work for you while you sleep. We’ve seen how a ₹1 lakh investment can become ₹1 crore, and how a 10-year head start can beat 25 years of playing catch-up.

If you’re a beginner in the Indian stock market, remember:

- Start a SIP, even if it’s small

- Stick to it religiously

- Don’t panic during downturns

- Choose the right funds (Growth option)

- Let time do its thing

By understanding and applying the power of compounding, you’re not just saving money — you’re building wealth.

Start today. Your future self will thank you.