If LTCG tax India 12.5 has you confused, that’s normal—because most people are trying to learn it from scattered headlines, half-remembered “old rules”, and WhatsApp forwards. The answer is: the rule is simple on paper, but most mistakes happen in application—especially when you sell multiple stocks, book profits across brokers, or mix equity with gold, debt, and property.

This confusion shows up everywhere—tax forums, broker support tickets, and Reddit threads where one comment says “no tax below ₹1.25 lakh” and the next says “it depends on regime, and exemption works differently.” And if you’re an active trader or a serious investor, even a small misunderstanding becomes expensive because it compounds over years: wrong tax calculation → wrong position sizing → wrong exit timing → avoidable penalties or missed opportunities.

StockManiacs has mentored thousands of Indian retail participants since 2008, and a pattern repeats every time rules change: traders focus on the rate (12.5%) and ignore the structure (what qualifies, what doesn’t, and how aggregation works across the financial year). This post fixes that with India-specific, practical guidance—built for people who actually buy and sell on NSE/BSE using Zerodha, Upstox, Fyers, and TradingView—not for textbook readers.

A quick promise before starting: no “sure-shot tips,” no fear-mongering, and no complicated jargon. This is a step-by-step guide to LTCG tax India 12.5 so that you can (1) calculate it correctly, (2) avoid common traps, and (3) use legal strategies like gain-harvesting without messing up your long-term tracking.

What exactly changed in LTCG tax India 12.5%?

Two decades of market cycles teach one thing: policy changes don’t hurt traders—confusion hurts traders. The answer is: listed equity LTCG is now taxed at 12.5% above an annual exemption of ₹1.25 lakh, and these rules apply to transfers made on or after 23 July 2024.

What the rule means (in plain English)

For most Indian investors, LTCG tax India 12.5 is about Section 112A assets—listed equity shares, equity-oriented mutual funds, and units of business trusts, where STT conditions apply. If your total long-term gains from these assets in a financial year are up to ₹1.25 lakh, the tax on that portion is effectively nil because of the exemption.

When gains cross ₹1.25 lakh, only the amount above ₹1.25 lakh is taxed at 12.5%. This is where many traders make the first big mistake: they apply the exemption “per stock” or “per trade,” instead of treating it as an annual, aggregated threshold.

What changed vs the older regime?

Earlier, Section 112A LTCG was 10% above ₹1 lakh; now it is 12.5% above ₹1.25 lakh, with the updated exemption applying for FY 2024-25 and later years. That change looks small, but it impacts anyone who books profits regularly—especially swing traders who exit multiple positions in a year.

A quick story (real-world pattern)

A trader books profits from 7 different stocks in a year, each time “keeping it under ₹1.25 lakh.” Then March arrives and the P&L statement shows total LTCG of ₹3.8 lakh across all sells. The exemption is still ₹1.25 lakh total—so tax applies on the remaining ₹2.55 lakh, not “zero because each trade was small.”

How do you calculate LTCG tax India 12.5 step by step?

Years of mentoring retail traders show that calculation errors usually come from skipping steps. The answer is: compute long-term gains first, aggregate them for the year, apply the ₹1.25 lakh exemption, then apply 12.5% on the balance (plus applicable cess/surcharge rules based on total income).

Step-by-step method (equity shares / equity MFs)

Use this workflow for LTCG tax India 12.5 on Section 112A assets:

- Step 1: Identify which sells qualify as LTCG (equity held > 12 months).

- Step 2: Compute gain per sell: Sale value minus cost of acquisition (and allowable expenses, if any).

- Step 3: Add all LTCG from the year (across all brokers).

- Step 4: Subtract ₹1.25 lakh exemption (once per year).

- Step 5: Tax = 12.5% of the remaining amount (then add cess/surcharge as applicable).

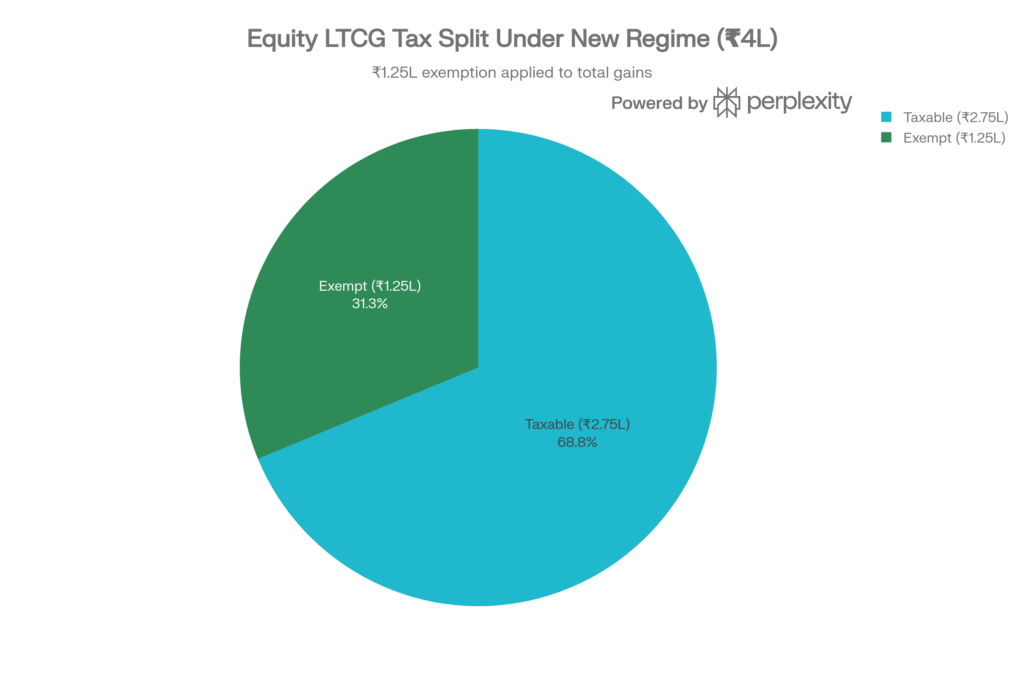

Example you can copy into your notes

Assume equity LTCG in FY 2025-26 is ₹4,00,000.

- Exempt: ₹1,25,000

- Taxable: ₹2,75,000

- Base tax: ₹34,375 (12.5% of ₹2,75,000)

This matches the standard computation approach explained in updated India tax guides and Section 112A explainers.

Why broker dashboards can mislead you

Broker apps are excellent for execution, not always for tax truth. A dashboard might show “Realized P&L” cleanly, but LTCG tax India 12.5 depends on holding period classification, corporate actions, and cross-platform aggregation. The safest habit is to treat broker reports as inputs and maintain a personal “tax ledger” (even a simple spreadsheet) for year-end verification.

Mini case: the “two-broker” trap

A trader uses Zerodha for delivery and a second broker for long-term smallcases. Both show LTCG under ₹1.25 lakh individually, so the trader assumes zero tax. But ITR requires aggregation, so the combined LTCG crosses ₹1.25 lakh and becomes taxable.

How can you legally reduce LTCG tax India 12.5?

Experience teaches that tax is not an enemy—randomness is the enemy. The answer is: reduce LTCG tax India 12.5 legally by planning exits, using the ₹1.25 lakh exemption intelligently, and avoiding strategy decisions that create unnecessary taxable events.

Strategy 1: Gain harvesting (the right way)

“Tax gain harvesting” means booking LTCG up to the exemption limit in a financial year and re-buying if the long-term thesis remains intact. This is popular on Indian mutual fund and tax communities because it can reset the cost price and use the exemption efficiently.

A clean approach:

- Identify long-term holdings where partial profit booking makes sense.

- Sell enough to realize LTCG up to (or near) ₹1.25 lakh.

- Re-enter only if the trade/investment still fits your system (not because of tax alone).

Warning: harvesting just to “save tax” can destroy compounding if it triggers overtrading, slippage, or emotional re-entry.

Strategy 2: Don’t create LTCG by accident

Many investors “upgrade” their portfolio monthly and end up selling winners too early. The better habit is to separate:

- Core long-term basket (low churn)

- Tactical swing basket (planned exits)

- High-frequency trading (business income/derivatives logic)

This reduces unnecessary exits and keeps your long-term book cleaner for LTCG tax India 12.5 planning.

Strategy 3: Plan your financial year exits

In India, the tax year matters as much as your chart. If you book profits on 31 March vs 1 April, the exemption bucket changes because it’s a new financial year. That single-day shift can decide whether you pay 12.5% now or later.

Real-world style scenario (what traders actually do)

A swing trader holds 12 quality stocks. In Feb–Mar, three stocks hit targets with large gains. Instead of exiting all three in March (and crossing the exemption), the trader exits two in March and one in April—purely to spread taxable LTCG across years. This is not “tax evasion”—it is timing within legal rules, as long as trades are genuine and properly reported.

What mistakes cost traders money under LTCG tax India 12.5?

Authority comes from seeing the same mistakes repeat across thousands of accounts. The answer is: the costliest mistakes are (1) mixing asset rules, (2) misunderstanding exemption vs regime, and (3) sloppy record-keeping that creates tax notices later.

Mistake 1: Assuming ₹1.25 lakh exemption applies everywhere

The ₹1.25 lakh exemption discussed under Section 112A is for listed equity/equity-oriented funds/business trust units under that section, not a universal “capital gains free pass.” This confusion shows up repeatedly in Indian tax discussions where people mix equity LTCG logic with other assets.

Practical check:

- If it’s not Section 112A, stop and re-check the tax section before applying the ₹1.25 lakh exemption.

Mistake 2: Confusing LTCG with trading income

If you do intraday equity, F&O, or frequent short holding delivery trades, the classification may shift toward business income depending on facts and consistency. Zerodha’s trader taxation guidance repeatedly emphasizes that turnover, intent, and consistency matter for how income is treated.

A simple mentor rule:

- If it behaves like a business, treat it like a business; don’t force-fit it into LTCG just because the rate looks lower.

Mistake 3: Ignoring the “effective date” reality

The CBDT FAQs clearly state the new capital gains provisions apply to transfers made on or after 23 July 2024. That means the sell date matters more than the buy date for which regime applies to the transfer.

Mini story: the painful “screen-shot proof” moment

A trader receives a query because the holding period was misread after a corporate action. The trader has the trading app screen-shot, but not the contract notes or consolidated statement. The fix becomes messy. The easiest prevention is boring: keep contract notes, CAS statements, and a simple spreadsheet of buys and sells.

How does LTCG tax India 12.5 affect your trading strategy?

A serious trader respects one truth: post-tax returns are the only returns that matter. The answer is: LTCG tax India 12.5 nudges many people toward fewer, higher-quality exits, and it changes how you compare delivery swing trades vs shorter-term trades taxed differently.

Delivery swing vs short-term churn: the real comparison

When people hear “12.5%,” they assume delivery is always superior. That’s not always true because:

- LTCG applies only after the holding period (equity > 12 months).

- Short-term exits don’t get the LTCG treatment and follow different rules/rates.

- Transaction costs, slippage, and the “mind tax” of frequent decision-making can outweigh nominal tax differences.

A trader who overtrades to “avoid tax” often pays more through poor execution than through tax. That pattern is visible in every market cycle.

A TradingView-style mindset shift (practical)

Instead of asking, “How can tax be zero?”, ask:

- “What is the cleanest system that produces the best post-tax, post-cost outcome?”

- “Can the strategy hold 12+ months for the best holdings?”

- “Can churn be reduced by upgrading entry filters (trend + fundamentals)?”

Hypothetical case: two traders, same skill

- Trader A exits winners every 3–6 months and re-enters often.

- Trader B holds winners for 18–36 months and trims only when structure breaks.

Trader B often pays less tax on a per-rupee-of-compounding basis because the system is built to let winners run, not because of “tax tricks.” LTCG tax India 12.5 rewards patience only when patience is backed by a process.

Where tools help (AmiBroker/Python approach)

A systematic trader can tag holdings by “age bucket” (0–6 months, 6–12, 12+), then plan exits with awareness of when LTCG eligibility begins. This is not complicated—just disciplined. That single dashboard view prevents accidental short-term exits right before the 12-month mark.

What should you do right now (before Budget season and year-end)?

Trust is built by giving a simple checklist that works in real life. The answer is: treat LTCG tax India 12.5 as a yearly planning problem—like risk management—so you don’t panic in March and you don’t guess while filing returns.

The “March-proof” LTCG checklist

Use this as a repeatable system:

- Pull consolidated capital gains reports from all brokers.

- Export your equity MF statements and match buy/sell dates.

- Create a one-page summary:

- Total LTCG (112A)

- Total STCG

- Total trading (intraday/F&O) turnover (if applicable)

- Exemption used (₹1.25 lakh bucket)

- If LTCG is close to ₹1.25 lakh, decide intentionally:

- book profits this year vs next year (only if the trade thesis supports it).

A simple table that prevents big confusion

| Question | Quick answer |

|---|---|

| “Is ₹1.25 lakh exemption per stock?” | No, it is an annual exemption bucket under Section 112A. |

| “Does 12.5% apply before 12 months?” | No, equity needs >12 months holding to be LTCG. |

| “Which date matters for new rules?” | Transfers on/after 23 July 2024 follow the updated provisions. |

Real customer voice (what people actually ask)

One common confusion posted on Indian tax communities is whether LTCG under 112A behaves differently under old vs new tax regime, and why someone still sees tax even when their total income looks “low.” Questions like that are signals: the rules are learnable, but only if you treat them like a system—not like trivia.

A practical “next step” for serious readers

If you want to be professional about this, do two things this week:

- Build a personal tax dashboard (even in Google Sheets).

- Decide a clear policy: “How often will profits be booked?” and “What qualifies as long-term holdings?”

That’s how you turn LTCG tax India 12.5 from a headache into a repeatable process.

Conclusion

Market experience since 2002 teaches a simple lesson: the government can change rules, but a trader’s job stays the same—protect capital, control risk, and build a repeatable process. The answer is: LTCG tax India 12.5 is manageable when you stop treating it like a one-time calculation and start treating it like a yearly system.

Here’s what matters most: listed equity/equity MF long-term gains are taxed at 12.5% only after you cross the ₹1.25 lakh annual exemption under Section 112A, and the updated provisions apply to transfers on or after 23 July 2024. Everything else—harvesting, timing, strategy selection—comes after you get this core correct.

It’s also worth being honest: tax planning is useful, but it should never push you into bad trades. A clean exit that protects your downside is better than “saving a little tax” and watching a winner turn into a loser. The best traders don’t optimize for tax alone—they optimize for post-tax outcomes, using fewer decisions, better filters, and calmer execution.

The strongest next step is practical: download your broker gain reports, aggregate across platforms, and write a one-page note for yourself—total LTCG, how much of the ₹1.25 lakh exemption is used, and what sells you might shift to the next financial year (only if the market structure and your plan allow it). Do that once, and you’ll feel the stress drop immediately because you’ll be operating with clarity, not assumptions.

Finally, a trust note: if any future links on StockManiacs point to broker partners, they may be affiliate links. The intent remains the same—education first, transparency always. For anything complex (large gains, mixed asset sales, business income classification), consult a qualified tax professional and keep your documentation tight.

When you treat LTCG tax India 12.5 like a system—just like risk management—you stop fearing it. You start using it.

")